Market Equilibrium Class 12 Extra Questions and Answers Free PDF Download

Free PDF download of Important Questions for CBSE Class 12 Micro Economics Chapter 5 - Market Equilibrium with Answers for prepared by expert Economics teachers from latest edition of CBSE(NCERT) books. Register online for Online tuition on Vedantu.com to score more marks in CBSE board examination.

Table of Content

Table of ContentA. Very Short Answer Questions - 1 Mark

1. What is a price taker firm?

Ans: A price taker firm is one that has no choice but to accept the industry's price due to their less transaction sizes. It has to agree to the price ascertained by the market forces.

2. What is a price maker firm?

Ans: A price maker firm is one that has the ability to influence prices on its own. A business with market power can increase prices without losing its consumers.

3. An individual firm under perfect competition cannot influence the market price, then who can and how?

Ans: Under perfect competition, the industry has the ability to affect market prices by increasing or decreasing output.

4. What is cooperative oligopoly?

Ans: Cooperative oligopoly occurs when firms in an oligopoly market cooperate with one another in deciding pricing and output.

5. What are advertisement costs?

Ans: Advertisement costs are the expenses made by a company to promote its sales, such as publicity through TV, radio, newspapers, magazines, and so on.

6. What is meant by normal profit?

Ans: Normal profit is the bare minimum of profit required to keep by an entrepreneur in business in the long run. The profit is higher than the opportunity cost that the business loses for utilizing their resources effectively.

7. What do you mean by abnormal profits?

Ans: When TR > TC, abnormal profit is a scenario for the firm. Abnormal profits are equivalent to a producer's gains in excess of its opportunity cost.

8. Why is AR equal to MR under perfect competition?

Ans: Under perfect competition, AR equals MR because the price is constant because the industry is the price maker and the businesses are the price taker. In this scenario, with the revenue for every additional unit of the product MR and AR will be the same to price.

9. What is the selling cost?

Ans: Selling cost is the expense incurred by a company for the promotion of a sale.

10. In which market form is there product differentiation?

Ans: Market with monopolistic competition there is product differentiation.

11. What do you mean by patent rights?

Ans: Patent rights are a company's exclusive right or permission to make a specified output using a specific technology. To get registered, all the information about that specific technology or process must be known to the public in patent application.

12. When a firm’s TR > TC, it cannot cover its normal profit

a) False

b) Can’t say

c) True

d) None of these

Ans: (a) False

13. The quantity to be sold by a firm under perfect competition is also fixed by the market.

a) True

b) Can’t say

c) None of these

d) False

Ans: (d) False

14. A firm maximizes its profits only when MR=MC

a) False

b) None of these

c) True

d) Cannot say

Ans: (c) True

15. Under perfect competition, market price can be influenced by both buyers and sellers.

a) True

b) False

c) None of the these

d) Cannot say

Ans: (b) False

B. Short answer Questions - 3 or 4 Marks

16. Explain two features of the monopoly market.

Ans: The following are the two most crucial characteristics of a monopoly market:

i. Sole Seller: As there is only one seller in the market, the seller can influence the market price on its own. A business with market power can increase prices without losing its consumers or competitors.

ii. High Entry Barrier: There exist entry hurdles for new enterprises, allowing sellers to earn abnormal profits that are far higher than usual earnings.

17. Why is the number of firms small in oligopoly? Explain.

Ans: The fundamental reason for the minimal number of firms in an oligopoly is that there exist barriers that restrict firms from entering the industry. Patents, huge capital requirements, and ownership over crucial raw materials, among other things, prohibit new firms from entering the industry. Only those who can overcome these obstacles will be able to enter and remain in the market.

Therefore, The numbers of firms are small in oligopoly.

18. Explain the implications of a large buyer in a perfectly competitive market?

Ans: A huge number of buyers are supposed to be so numerous that an individual buyer's percentage of total purchases is so insignificant that he cannot influence market price by purchasing more or less. As a result, the pricing remains unchanged.

Every business in the industry would be earning only normal profits due to the large number of buyers. The buyers are the price takers and have no bargaining power in the market.

19. Explain the implications of the following:

a) Interdependence between firms in oligopoly

b) Large number of sellers in perfect competition

Ans: The implications of the above features are as follows

a) Oligopolies are often made up of a few huge corporations. Because each firm is so huge, its actions have an impact on market circumstances. As a result, rival firms will be aware of a firm's market activity and will respond properly. Mutual interdependence develops when one firm's actions have a significant impact on the other enterprises in the industry.

b) The presence of a large number of buyers and sellers of a commodity dominates a fully competitive market, which implies that there is no such buyer or seller in the market whose purchase or sale is so huge that it affects the overall sale or purchase in the market. Each buyer/seller owns only a little portion of the market demand/supply.

20. Explain briefly why a firm under perfect competition is a price taker not a price maker?

Ans: Because the price is set by market forces of demand and supply, a firm in perfect competition is a price taker rather than a price maker. This is referred to as the equilibrium price. At this equilibrium price, all firms in the industry must sell their outputs. The reason for this is that the number of enterprises in perfect competition is so high. As a result, no firm's supply can impact the price. Every company makes the same type of goods.

C. Long Answer Questions - 6 Marks

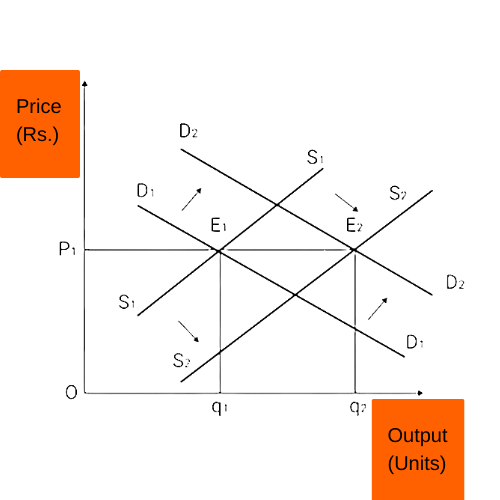

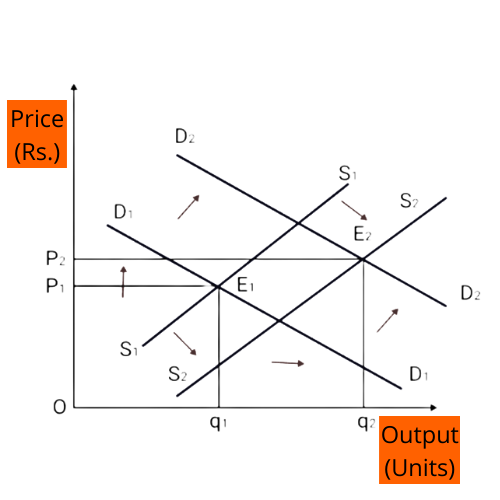

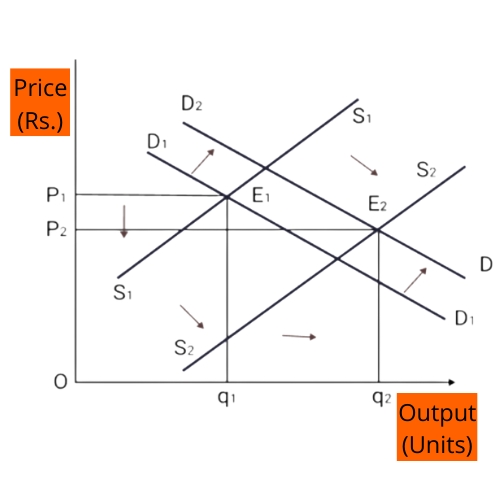

21. Market for a good is in equilibrium. There is simultaneous increase both in demand and supply of the goods. Explain its effects on market price.

Ans: When there is no motivation for a condition to alter, equilibrium exists. When equilibrium is reached, the amount of goods that customers intend to buy equals the number of goods that producers intend to sell. The market moves to equilibrium due to the rules of demand and supply. The effect of increased demand and supply on equilibrium price and quantity is explored in three separate cases:

i. When increase in demand is equal to increase in supply: When demand increases proportionately to supply increases, the rightward shift in the demand curve from

D1D1 to D2D2 is correspondingly equal to the rightward shift in the supply curve from S1S1 to S2S2 . E2 determines the new equilibrium. Because both demand and supply grow in the same proportion, the equilibrium price remains constant at OP1 . while the equilibrium quantity increases from Oq1 to Oq2 .

ii. When increase in demand is greater than increase in supply: When demand increases more than supply increases, the rightward shift in the demand curve from D1D1 to D2D2 is proportionately greater than the rightward movement in the supply curve from S1S1 to S2S2 . The new equilibrium is found at E2 , where the equilibrium price rises from OP1 to OP2 and the equilibrium quantity rises from Oq1 to Oq2 .

iii. When demand increases but less than increase in supply: When demand increases less than supply increases, the rightward shift in the demand curve from D1D1 to D2D2 is proportionately less than the rightward movement in the supply curve from S1S1 to S2S2 . The new equilibrium is determined at E2 . The equilibrium price decreases from OP1 to OP2 while the equilibrium quantity increases from Oq1 to Oq2 .

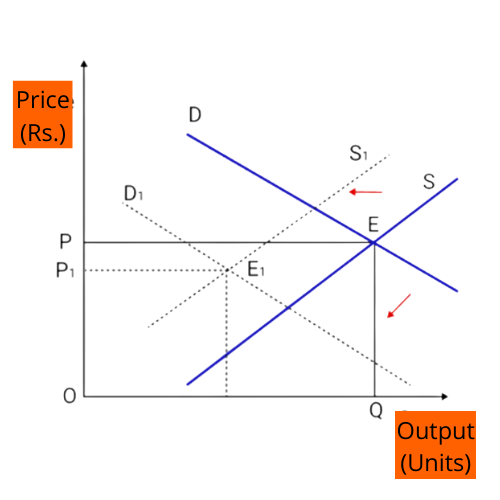

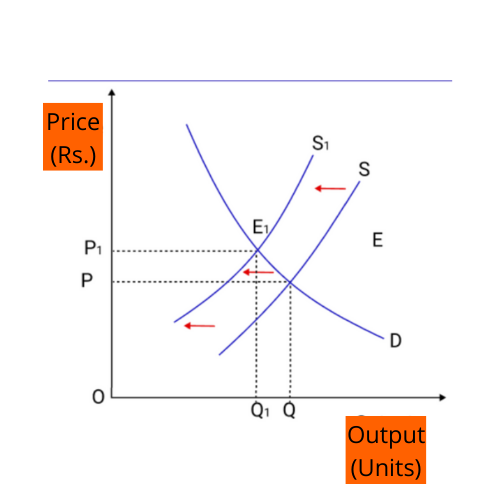

22. Market for a good is in equilibrium. There is simultaneous decrease both in demand and supply, but there is no change in the market price. Explain with the help of diagram, how it is possible.

Ans: When the decline in demand exceeds the decrease in supply, the market price does not change. When the decrease in demand is greater than the decrease in supply, the leftward shift in the demand curve from D to D1 is greater than the leftward shift in the supply curve from S to S1 The new equilibrium is established at E2 , the equilibrium price shifts from OP to OP1 , and the equilibrium quantity shifts from OQ to OQ1

23. How does an equilibrium price and an equilibrium quantity of a normal commodity be affected by an increase in an income of the buyers? Explain with the help of a diagram.

Ans: When a consumer's income rises, the demand curve for ordinary products shifts to the right. The supply curve is unaltered. However, when consumers are prepared to pay a greater price for the same quantity or when their income rises. This will cause the price to soar. As a result, the quantity supplied by the producers would likely increase.

Thus, a rise in demand and the resulting shift in the demand curve to the right affects producer decisions by extending supply in response to a price increase. Finally, you would arrive at a situation in which an equilibrium price and an equilibrium quantity tend to rise in response to an increase in demand.

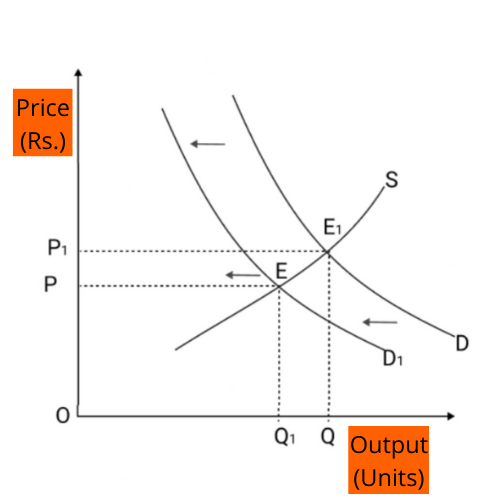

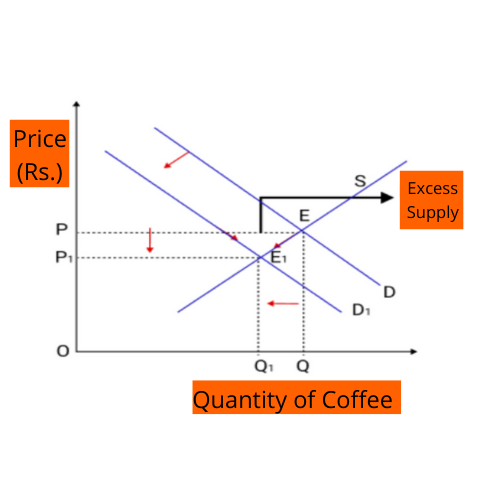

24. How a fall in the price of tea will affect an equilibrium price of coffee? Explain the chain effects.

Ans: As the price of tea falls, so does the demand for coffee, which is an alternative to tea. As a result, the coffee demand curve changes to the left. As a result, an equilibrium price tends to fall and an equilibrium quantity tends to fall.

The graph depicts a declining demand condition. The demand curve swings to the left. As a result, both the equilibrium price and quantity are lowering from OP to OP1 and OQ to OQ1

Due to the fall in the price of tea:

i. The Equilibrium price of coffee drops from OP to OP1

ii. The equilibrium quantity also drops from

OQ to OQ1

Important Study Material Links for Class 12 Microeconomics Chapter 5

CBSE Class 12 Economics Important Questions Textbooks

Chapter-wise Links for Microeconomics Class 12 Questions

Related Study Materials Links for Class 12 Microeconomics

Along with this, students can also download additional study materials provided by Vedantu for Microeconomics Class 12–

FAQs on Important Questions For Class 12 Micro Economics Chapter 5 Market Equilibrium - 2026-27 PDF Download (Login Required)

1. What is market equilibrium, and how is it determined as per the Class 12 Economics syllabus?

Market equilibrium is the state where the quantity demanded equals the quantity supplied at a particular price. It is determined by the intersection of the demand and supply curves, ensuring there is no tendency for further change in price or quantity in that market, according to the CBSE 2026–27 Economics syllabus.

2. Explain three key factors that can disturb market equilibrium in Class 12 Economics context.

The major factors that can disturb market equilibrium include:

- Change in demand due to shifts in consumer income or preferences

- Change in supply caused by input cost fluctuations or technological advancements

- Government interventions such as taxes, subsidies, or price controls

3. In CBSE Class 12 exams, how is equilibrium price affected if both demand and supply increase simultaneously?

If demand and supply both increase at the same time, the equilibrium quantity definitely rises, but the effect on equilibrium price depends on the relative magnitude of the shifts:

- If demand increases more than supply, price rises.

- If supply increases more than demand, price falls.

- If both increase equally, price remains unchanged.

4. Why is a perfectly competitive firm called a ‘price taker’ in Class 12 market equilibrium questions?

In a perfectly competitive market, individual firms are called ‘price takers’ because they sell products that are identical to those sold by other firms and cannot influence the market price. The price is set by overall market forces of demand and supply, as per CBSE Class 12 guidelines.

5. Describe one ‘5-mark’ HOTS question on how market equilibrium is restored after a sudden fall in supply, referencing recent board trends.

When supply unexpectedly drops, there is initially excess demand at the original price. This leads to competition among buyers, pushing up the price. As price rises, quantity demanded falls and quantity supplied rises (producers are incentivized). The process continues until a new equilibrium is achieved at a higher price and lower quantity. CBSE often asks this as a ‘chain of effects’ in board exams.

6. State two commonly tested differences between market equilibrium under perfect competition vs monopoly for Class 12 important questions.

- Perfect Competition: Price equals marginal cost at equilibrium; firms are price takers. Equilibrium is determined by market demand and supply.

- Monopoly: Price is set above marginal cost; monopolist as a price maker. Equilibrium is determined where marginal revenue equals marginal cost for the single producer.

7. What is the significance of abnormal profits in the context of market equilibrium for Class 12 board exams?

Abnormal profits refer to profits exceeding normal earning levels (over and above opportunity cost). In the long-run equilibrium of a perfectly competitive market, abnormal profits attract new firms, which increases supply and reduces price, restoring only normal profits. Board questions often use this to test knowledge of equilibrium adjustment.

8. How do indirect taxes affect market equilibrium as per Class 12 CBSE expectations?

The imposition of an indirect tax (such as GST) increases the cost for producers, resulting in a leftward shift of the supply curve. This leads to a higher equilibrium price and lower equilibrium quantity. Understanding diagrammatic representation is essential for scoring in application-based questions.

9. Outline the stepwise method to solve a numerical on market equilibrium as typically required in CBSE Class 12 exams.

- Write down the given demand and supply equations (e.g., Qd = 100 - 10P, Qs = 20 + 15P).

- Set Qd = Qs and solve for P (the equilibrium price).

- Substitute P back into either equation to find the equilibrium quantity.

- Double-check units and ensure steps align with the CBSE answer key format.

10. What are the implications if equilibrium in a market is not achieved, with reference to Class 12 important questions?

If equilibrium is not achieved, there is either excess demand or excess supply. Excess demand leads to rising prices; excess supply results in falling prices. Persistent disequilibrium can create black markets or unsold inventories. Understanding these effects satisfies both 3-mark and 5-mark question types as per the 2026–27 syllabus.

11. FUQ: How can misconceptions about the law of equilibrium cause errors in exam answers, and how should students avoid them?

Common misconceptions include assuming only price changes restore equilibrium or confusing movement along curves with shifts of curves. Students should:

- Clearly distinguish between shifts vs movements.

- Justify adjustment mechanisms using both price and quantity changes.

- Carefully read what is being changed: variables vs constants.

12. FUQ: Compare the adjustment speeds of equilibrium in perishable vs durable goods markets, following HOTS format.

Perishable goods (like vegetables) tend to find equilibrium faster due to the inability to store excess supply; prices fall quickly if unsold. Durable goods (like cars) can be stored, so sellers may wait for better prices, resulting in slower adjustment. This application-focused comparison is frequently used in CBSE HOTS questions.

13. FUQ: What ‘blind spots’ in board answers should students avoid when diagramming market equilibrium scenarios?

Students often miss correct labelling of curves, axes, and equilibrium points, or forget to indicate direction of shifts. For full marks, always:

- Label Demand (D) and Supply (S) curves clearly

- Mark initial and new equilibrium points

- Show direction of curve shifts

14. FUQ: Suggest a structured approach to answer ‘explain with diagram’ 5-mark questions on simultaneous changes in demand and supply in recent CBSE papers.

Begin by outlining the case (increase/decrease in both demand and supply). Draw the original and new curves on the same graph, marking equilibrium shifts. State clearly whether the price, quantity, or both changes, and support each conclusion with reference to the diagram. End with a concise summary, aligning to 5-mark CBSE board expectations.

15. Why is studying market equilibrium important in Class 12 CBSE Economics?

Understanding market equilibrium is fundamental because it explains how prices and output are determined in free markets, predicts the effects of policy or external shocks, and forms the basis for more advanced economic analysis, as outlined in the 2026–27 CBSE syllabus.