An Overview of Important Questions Class 12 Micro Economics Chapter 4

Ever wondered how markets actually work? In Theory of the Firm under Perfect Competition Important Questions for Class 12 Economics, you’ll dive into the world of market structures, price setting, and what it takes for a firm to survive in a competitive world. You’ll get to understand important ideas like perfect competition, monopoly, and how firms decide how much to produce and sell.

Table of Content

Table of ContentThese questions are picked from the latest syllabus and are great for clearing up common confusion on producer’s equilibrium, demand-supply, and the logic behind why some firms make profits while others exit the market. Curious about what else you need to study? Take a look at the updated Class 12 Economics Syllabus for a full overview.

Practicing these Vedantu Important Questions—with their handy PDF download—can really boost your confidence for exams. For even more practice, check out all the Class 12 Economics Important Questions you need.

Very Short answer Questions (1 or 2 Marks)

1. Define perfect competition.

Ans: A market with perfect competition has a large number of customers and sellers selling the same product at the same price.

2. Define Monopoly.

Ans: A monopoly is a market arrangement in which a single supplier has complete price control.

3. Condition for producer equilibrium is

a) TR=TVC

b) MC=MR

c) None of above

d) TC=TSC

Ans: (b) MC=MR

4. ____________ is an ideal market?

a) Monopolistic competition

b) Oligopoly

c) Monopoly

d) Perfect competition

Ans: (d) Perfect competition

5. Under which market situation demand curve is linear and parallel to X-axis?

a) Monopoly

b) Perfect competition

c) Oligopoly

d) Monopolistic competition

Ans: (b) Perfect competition

6. If under perfect competition, the price lies below the average cost curve, the firm would?

a) Incur losses

b) Make abnormal profits

c) Make only normal profits

d) Profit cannot be determined

Ans: (a) Incur losses

7. What are the conditions for the long run equilibrium of the competitive firm?

a) P=MR

b) LMC=LAC=P

c) SMC=SAC=LMC

d) All of the above

Ans: (b) LMC=LAC=P

8. A firm can sell as much as it wants at the market price. The situation is related to?

a) Monopoly

b) Monopolistic competition

c) Perfect competition

d) Oligopoly

Ans: (c) Perfect competition

9. What is oligopoly?

Ans: Oligopoly is defined as a market structure characterized by a small number of significant sellers who sell either homogeneous or differentiated commodities.

10. What is product differentiation?

Ans: It is the practice of differentiating products and services on various basis such as style, looks, label, color, size, packaging, brand name, etc., with an objective to make it more attractive and better than the product or service of the competitors.

11. What is the shape of marginal revenue curve under monopoly?

Ans: In a monopoly market, the marginal revenue curve slopes downhill from left to right and is lower than the average revenue curve.

12. What is break – even price?

Ans: The break-even price in a completely competitive market is the price at which a firm earns normal profit (Price =AC ). In the long run, the break-even price is the point at which P=AR=MC.

13. Globalization has made Indian Market as?

a) Buyer market

b) Monopsony market

c) Seller market

d) Monopoly market

Ans: (a) Buyer market

14. When AR=Rs.10 and AC= Rs. 8 the firm makes?

a) Gross profit

b) Normal profit

c) Net profit

d) Supernormal profit

Ans: (d) Supernormal profit

15. A competitive firm in the short run incurs losses. The firm continues production, if?

a) $\mathrm{P}>\mathrm{AVC}$

b) $\mathrm{P}=\mathrm{AVC}$

c) $\mathrm{P} \geqslant \mathrm{AVC}$

d) $\mathrm{P}<\mathrm{AVC}$

Ans: (c) $\mathrm{P} \geq \mathrm{AVC}$

Short Answer Questions - 3 or 4 Marks

16. Why is the demand curve in monopolistically competitive firms likely to be very elastic?

Ans: The demand curve in monopolistically competitive firms is likely to be very elastic. The reason for this is because the products produced by monopolistically competitive enterprises are nearly identical, and the firms have less control over the price. If the items are close replacements of one another, and the product is not differentiated enough, the elasticity of demand becomes strong, making the firm's demand curve very elastic.

17. Explain the implication of free entry and free exit of a firm in a perfect competitive market?

Ans: If firms can enter and exit freely, no firm can achieve an extraordinary profit in the long run. That is, the corporation earns no extraordinary profit in case of freedom of entry and exit, and hence, each company gets a standard profit. In a perfect competition there are large numbers of buyers and sellers.

‘Free Entry’ means that there are no obstacles in the entry of new firms in the market. When the existing businesses are earning abnormal profits, the new firms are influenced due to the profit and they enter the industry. This increases market supply which leads to fall in market price and furthermore profits.

'Freedom to exit' means that there are no obstacles which stop the existing firms from stepping down from the market. The firms attempt to quit when they are dealing with losses. As the firms start to exit, market supply drops, which begins to rise in market price and consequently decreases in losses. The firms do not stop to leave till the losses are eliminated and each remaining firm will be earning just the normal profits.

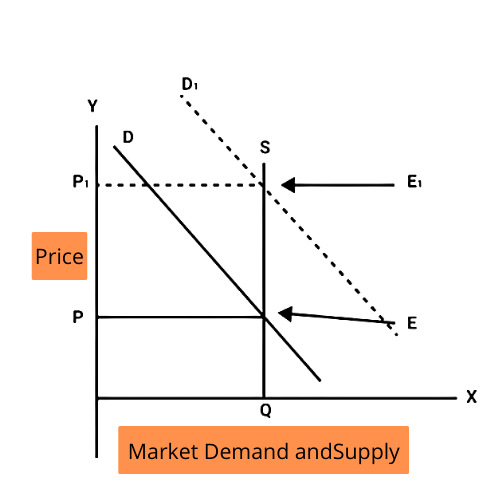

18. With the help of the diagram, show the effect on equilibrium price and quantity when supply is perfectly inelastic and demand increases & decreases.

Ans: Rise in Demand

When supply is completely inelastic and demand rises, the demand curve shifts to the right. At point, the new demand curve intersects the supply curve at point As a result, prices rise whereas quantity demand remains unchanged.

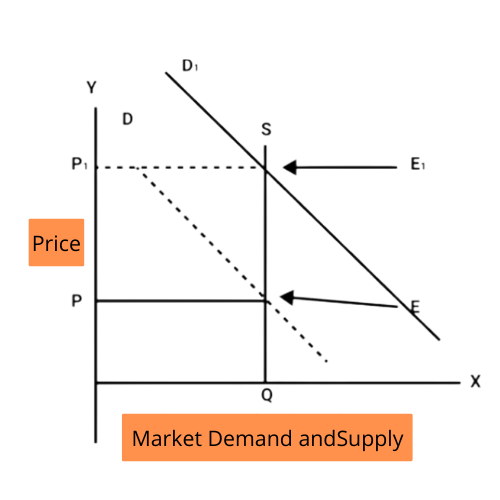

Fall in Demand

In the diagram shown below, demand curve shifts towards left when demand falls and price decreases from but quantity remains same.

19. Which features of monopolistic competition are monopolistic in nature?

Ans: Monopolistic competition refers to a market situation in which there are a large number of firms selling products that are closely related but distinct.

Large number of sellers: There are a large number of businesses selling products that are related but not identical. Each firm operates independently and has a limited market share. As a result, a single firm has only limited control over the market price. The presence of a large number of businesses creates market competition.

Product Differentiation: Despite the large number of sellers, each firm can exercise some degree of monopoly through product differentiation. Product differentiation is the process of distinguishing products based on their brand, size, color, shape, and so on. A firm's product is a close but not perfect substitute for another firm's product.

Selling costs: Products are differentiated in monopolistic competition, and these differences are communicated to buyers through selling costs. The expenses incurred on marketing, sales promotion, and product advertisement are referred to as selling costs.

Freedom of entry and exit: Firms are free to enter or exit the industry at any time under monopolistic competition. It ensures that a firm does not experience abnormal profits or losses in the long run.

Lack of perfect knowledge: Buyers and sellers do not have a complete understanding of market conditions. Selling costs create an artificial superiority in the minds of consumers, making it difficult for them to evaluate different products on the market. As a result, even if other less expensive products are of equal quality, consumers prefer a specific product (even if it is highly priced).

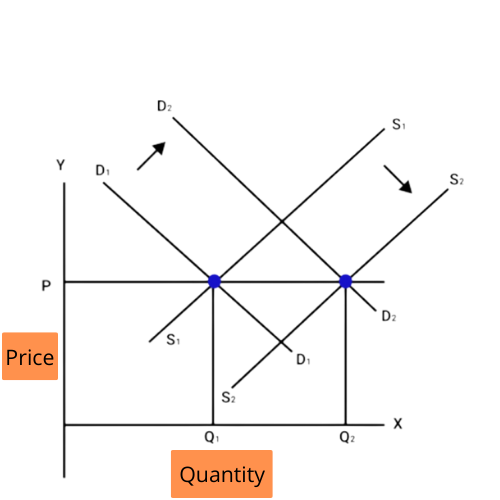

20. When will the equilibrium price not change even if demand and supply increases?

Ans: When the proportionate rise in demand is exactly equal to the proportionate increase in supply, the equilibrium price remains constant. It is depicted in the diagram below.

Diagram

In this diagram one can see that when both demand and supply increase at an equal level. The price remains unchanged, even though the quantity changes.

Long Answer Questions (5 or 6 Marks)

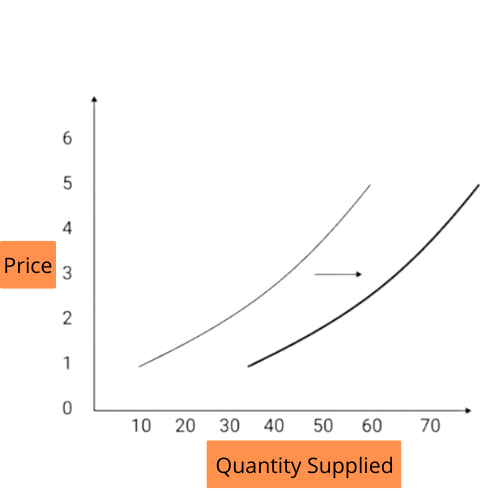

21. Distinguish between change in supply and change in quantity supplied. State two factors responsible for change in supply.

Ans: The difference between change in supply and change in quantity supplied is as follows:

Difference in Diagrams - Change in Supply:

The change in supply is depicted in the graphic below. We can see an increase in supply due to reasons other than price, shown through rightward movement.

Difference in Diagrams - Change in Quantity Supplied:

A change in quantity delivered would be depicted as an upward movement in the supply curve due to an increase in price.

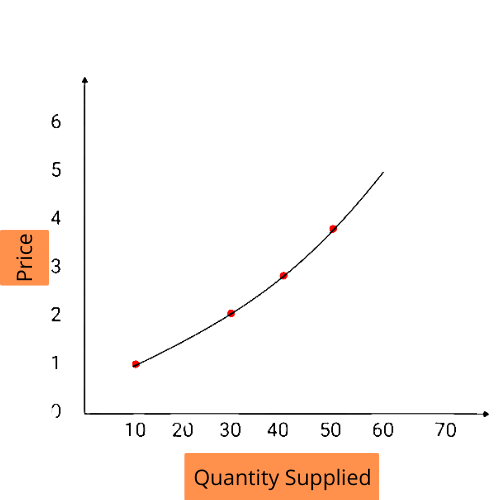

Take note that this is the supply curve that has been separated on the graph. A distinct quantity is delivered at each point on the curve. So, if we shift from $\mathrm{p}=1$ to $\mathrm{p}=2$, the quantity delivered changes by 20 units because we went from $\mathrm{q}=10$ at $\mathrm{p}=1$ to $\mathrm{q}=30$ at $\mathrm{p}=2$.

As a result, changes in supply allow manufacturers to sell more (or less) at a given price. Changes in amount supplied, on the other hand, are induced by price changes, causing manufacturers to sell more (or less) at a different price.

Factors are responsible for changes in supply:

Production costs: Input prices and the consequent production costs are inversely related to supply. Changes in input prices and production costs, in other words, create an opposing shift in supply. For example, as wages or labor expenses rise, the supply of goods falls.

Technology: Improvements in manufacturing technology change the supply curve. Improvements in technology, in particular, boost supply, resulting in a rightward shift in the supply curve, that is better the technology, higher the supply.

Other goods prices: Other items' price adjustments are a little more challenging. To begin, in order to influence supply, producers must believe the items are related. What customers believe is unimportant. Ranchers, for example, believe that meat and leather are connected since they both come from a steer.

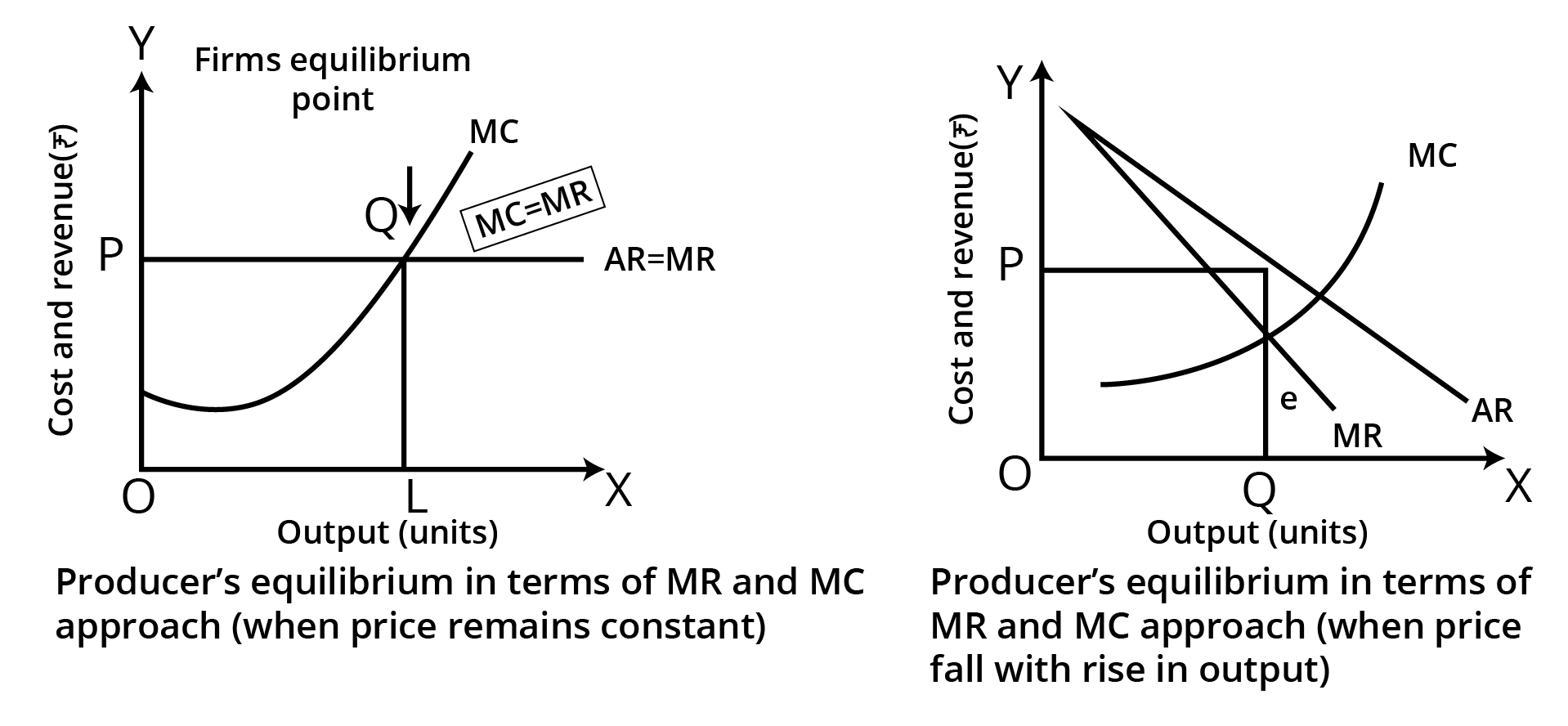

22. Explain the conditions of a producer’s equilibrium in terms of Marginal Cost and Marginal Revenue. Use a diagram.

Ans: The term "producer's equilibrium" refers to a condition in which a producer produces the amount of output that maximizes earnings. It is a profit-maximizing condition. Under the MR-MC technique, the producer will only reach equilibrium at the level of production if the following conditions are met.

MR = MC

After MR = MC, MC must rise.

At the point of equilibrium, the MC curve must cut the MR curve from below.

The addition to TR from the sale of one additional unit of output is denoted by MR, and the addition to TC is denoted by MC. Firms compare their MR with their MC in order to maximize earnings.

In the diagram, output is indicated on the $X$ axis, while revenue and cost are shown on the Y-axis. The MC curve is U-shaped, and $P \sim M R=A R$ is a horizontal line parallel to the X-axis.

When output level is more than OQ, MR < MC, which implies that the firm is making a loss on its last unit of output. Hence, so as to maximize profit, a rational producer will keep decreasing its output as long as MC >MR. Thus, the firm moves towards producing OQ units of output.

23. When the price of a commodity rises from Rs. 10 to Rs. 11 per unit, its quantity supplied rises by 100 units. Its price elasticity of supply is 2. Calculate its quantity supplied at the increased price.

Ans: Given:

P=10

P1=11

$\Delta \mathrm{Q}=100 \mathrm{units}$

$\mathrm{E}_{\mathrm{s}}=2$

$\Delta \mathrm{P}=\mathrm{P}_{1}-\mathrm{P}$

$\quad=11-10$

$\quad=1$

The price elasticity of supply is calculated as

$\mathrm{E}_{\mathrm{s}}=\dfrac{\Delta \mathrm{Q}}{\Delta \mathrm{P}} \times \dfrac{\mathrm{P}}{\mathrm{Q}}$

Substitute the known values in the above equation,

$2=\dfrac{100}{1} \times \dfrac{10}{\mathrm{Q}}$

$\mathrm{Q}=\dfrac{100 \times 10}{2}=500$

Therefore, the quantity supplied at the increase price is calculated as

$\mathrm{Q}_{1} =\mathrm{Q}+\Delta \mathrm{Q}$

$=500+100$

$=600 \text { units }$

24. A firm supplies 500 units of a good at a price of Rs. 5 per unit. The price elasticity of supply of good is 2. At what price will the firm supply 700 units?

Ans: Given:

$\mathrm{P}=5$

$\mathrm{Q}_{1}=700$

$\mathrm{Q}=500$

$\mathrm{E}_{\mathrm{s}}=2$

$\Delta \mathrm{Q}=\mathrm{Q}_{1}-\mathrm{Q}$

$=700-500=200$

The price elasticity of supply is calculated as

$\mathrm{E}_{\mathrm{s}}=\dfrac{\Delta \mathrm{Q}}{\Delta \mathrm{P}} \times \dfrac{\mathrm{P}}{\mathrm{Q}}$

Substitute the known values in the above equation,

$2=\dfrac{200}{\Delta \mathrm{P}} \times \dfrac{5}{500}$

$\Delta \mathrm{P}=\dfrac{2 \times 500}{200 \times 5}=1$

Therefore, the new price is calculated as

$\mathrm{P}_{1}=\mathrm{P}+\Delta \mathrm{P}$

$=5+\mathrm{l}$

$=6 \text { units }$

Therefore, the firm will supply 700 units at Rs. 6 per unit.

Important Study Material Links for Class 12 Microeconomics Chapter 4

CBSE Class 12 Economics Important Questions Textbooks

Chapter-wise Links for Microeconomics Class 12 Questions

Related Study Materials Links for Class 12 Microeconomics

Along with this, students can also download additional study materials provided by Vedantu for Microeconomics Class 12–

FAQs on Important Questions For Class 12 Micro Economics Chapter 4 Theory of the Firm under Perfect Competition - 2026-27 Free PDF Download (Sign-in Required)

1. What are the main characteristics of a perfectly competitive market, as expected in Class 12 board exams (CBSE 2026–27)?

- Large number of buyers and sellers: No single buyer or seller can influence market price.

- Homogeneous products: All firms sell identical goods.

- Free entry and exit: Firms can join or leave the market without barriers in the long run.

- Perfect information: Buyers and sellers have complete knowledge of prices and products.

- No selling costs: No advertising or promotions needed since products are identical.

2. Explain the condition of producer equilibrium under perfect competition for Class 12 Economics.

Producer equilibrium in a perfectly competitive market is achieved when Marginal Cost (MC) equals Marginal Revenue (MR), and the MC curve cuts the MR curve from below. This ensures the firm maximizes its profit. No additional unit of output will add to profit after this point.

3. Why are firms unable to earn abnormal profits in the long run under perfect competition? (CBSE HOTS)

- Free entry of new firms: Any short-term abnormal profit attracts new entrants.

- This increases market supply, leading to a fall in price until only normal profit is possible.

- Losses also force firms to exit, reducing supply and restoring normal profits.

4. How does the demand curve faced by an individual firm under perfect competition differ from that in a monopoly?

Under perfect competition, a firm's demand curve is perfectly elastic (horizontal to the x-axis), since it can sell any quantity at the market price. In monopoly, the firm's demand curve is downward sloping, allowing the firm to set price by adjusting output.

5. What is the significance of 'normal profit' for a competitive firm in the long run as per CBSE 2026–27 mark scheme?

- Normal profit is the minimum earning required to keep an entrepreneur in business.

- In the long run, perfectly competitive markets ensure all firms earn only normal profits due to free entry and exit.

6. Under what condition will a perfectly competitive firm continue to operate even if it is making a loss in the short run? (application-based for 3/4 mark)

The firm will continue to operate if the price is greater than or equal to Average Variable Cost (P ≥ AVC). Shutting down would be considered only if price falls below AVC.

7. What happens to equilibrium price and quantity if both demand and supply increase by the same proportion in a perfectly competitive market?

If both demand and supply increase by the same proportion, the equilibrium price remains unchanged, but the equilibrium quantity increases.

8. Distinguish between change in supply and change in quantity supplied with relevant CBSE examples. (5-mark)

- Change in supply: Occurs due to factors other than price (e.g. technology, input costs), shifting the supply curve right or left.

- Change in quantity supplied: Caused only by change in price, shown as a movement along the supply curve.

- Example: If wage rates fall (input cost decrease), the supply curve shifts (change in supply); if price of the product increases, movement occurs along the curve (change in quantity supplied).

9. How does product differentiation distinguish monopolistic competition from perfect competition? (Frequently Asked, 3-mark)

In monopolistic competition, firms differentiate products by style, brand, or features, allowing some price influence. In perfect competition, products are identical, so firms are price takers with no differentiation.

10. Explain the importance of the MC=MR rule in determining the profit-maximizing output for a firm in perfect competition.

The MC=MR rule ensures resources are used efficiently. The firm maximizes profit by producing up to the point where the cost of producing one more unit equals the revenue it generates. Beyond this point, producing more would lower profit.

11. What are some common misconceptions about price determination under perfect competition? (FUQ; exam traps)

- Believing individual firms set the market price (actually, the price is set by market forces of demand and supply).

- Assuming abnormal profits are possible in the long run (only normal profits occur due to free entry/exit).

- Thinking products may be differentiated (in fact, all firms sell identical products).

12. Why is the supply curve of a perfectly competitive firm the part of its marginal cost curve above AVC?

This segment represents the minimum price at which a firm is willing to produce, since selling below AVC would result in losses greater than fixed costs, leading the firm to shut down in the short run.

13. Using CBSE 2026–27 exam approach, what are the long-run equilibrium conditions for a perfectly competitive firm?

- Price = Marginal Cost = Average Cost (P = MC = AC).

- Firms earn only normal profit.

- Entry and exit have stopped; no incentive for further firms to enter or leave.

14. What if a perfectly competitive firm's average revenue exceeds its average cost? (Numerical-based HOTS)

If Average Revenue (AR) > Average Cost (AC), the firm is making supernormal (abnormal) profit in the short run. This situation cannot persist in the long run.

15. How are price elasticity of supply and producer behavior related in perfect competition? (Expected conceptual)

- A higher price elasticity of supply means producers can quickly adjust production in response to price changes.

- In perfect competition, individual firms are highly responsive to price changes, leading to a typically elastic supply curve in the long run.