Business Studies Notes for Chapter 8 Controlling Class 12 - FREE PDF Download

Chapter 8 on Controlling in Class 12 gives insights into the vital managerial function of controlling. It emphasises the importance of measuring performance against set standards and correcting deviations to ensure that organisational objectives are met. This chapter highlights how effective controlling supports goal achievement, resource management, and employee motivation, while also addressing its limitations. Understanding these aspects is crucial for managing and guiding an organisation toward its strategic goals.

Table of Content

Table of ContentChapter 8 Controlling Notes allows you to access and review the chapter content quickly. for a comprehensive study experience, check out the Class 12 Business Studies Notes FREE PDF here and refer to the Class 12 Business Studies Syllabus for detailed coverage. Vedantu's notes offer a focused, student-friendly approach, setting them apart from other resources and providing you with the best tools for success.

New Updations of Class 12 Chapter 8 Controlling

Definition

“Managerial Control implies the measurement of accomplishment against the standard and the correction of deviations to assure attainment of objectives according to plans.”

Koontz and O'Donnell.

Meaning

Controlling is a process that entails comparing actual performance to the desired outcome, to ensure the achievement of objectives. Setting standards, measuring actual performance, and taking corrective action in case of deviations are all part of the managerial role of controlling function.

Importance of Controlling

Achieving Organisational Goals: Tracks progress towards objectives and addresses deviations to ensure goals are met.

Judging Accuracy of Standards: Assesses the accuracy of standards by monitoring changes in the environment.

Making Efficient Use of Resources: Minimises resource waste through effective resource management.

Improving Employees’ Motivation: Clarifies expectations and performance requirements, motivating employees to perform better.

Ensuring Order and Discipline: Creates an orderly and disciplined work environment through careful monitoring.

Facilitating Coordination in Action: Ensures all departments and employees follow set standards and goals, promoting overall coordination.

Limitations of Controlling

Difficulty in Setting Quantitative Standards: When standards are hard to measure, the effectiveness of the control system diminishes.

Little Control on External Factors: Factors such as government regulations, technological changes, and competition are beyond the organisation's control.

Resistance from Employees: Employees may resist being controlled or monitored, which can lead to decreased morale and conflicts.

Costly Affair: Implementing and maintaining control systems can be expensive, requiring substantial financial, time, and resource investments.

Features of Controlling

Goal-Oriented: Helps to achieve defined goals or objectives, determining the success of management efforts.

Pervasive: Necessary in all organisations (profit, non-profit, business, or non-business) and at all management levels (top, middle, lower).

Continuous: Involves ongoing performance assessment and improvement to align and support staff development and success.

Reviews Staff Performance: Monitors performance, dedication, and issues within the staff through the controlling function.

forward-Looking: Helps in planning future actions if actual performance deviates from set standards.

Dependent on Planning: This relies on planning, as it compares actual performance against planned performance.

Action-Oriented: Focuses on effective coordination of resources to achieve organisational objectives through supervision and action by staff.

Relationship Between Planning and Controlling

Planning Requires Control: Effective control is based on predefined standards set by planning. Without plans, control lacks direction.

Control Validates Planning: Control ensures plans are effective by detecting deviations and implementing corrective measures.

Control Assesses Planning Efficiency: By evaluating performance against plans, controlling helps refine and adjust plans and actions.

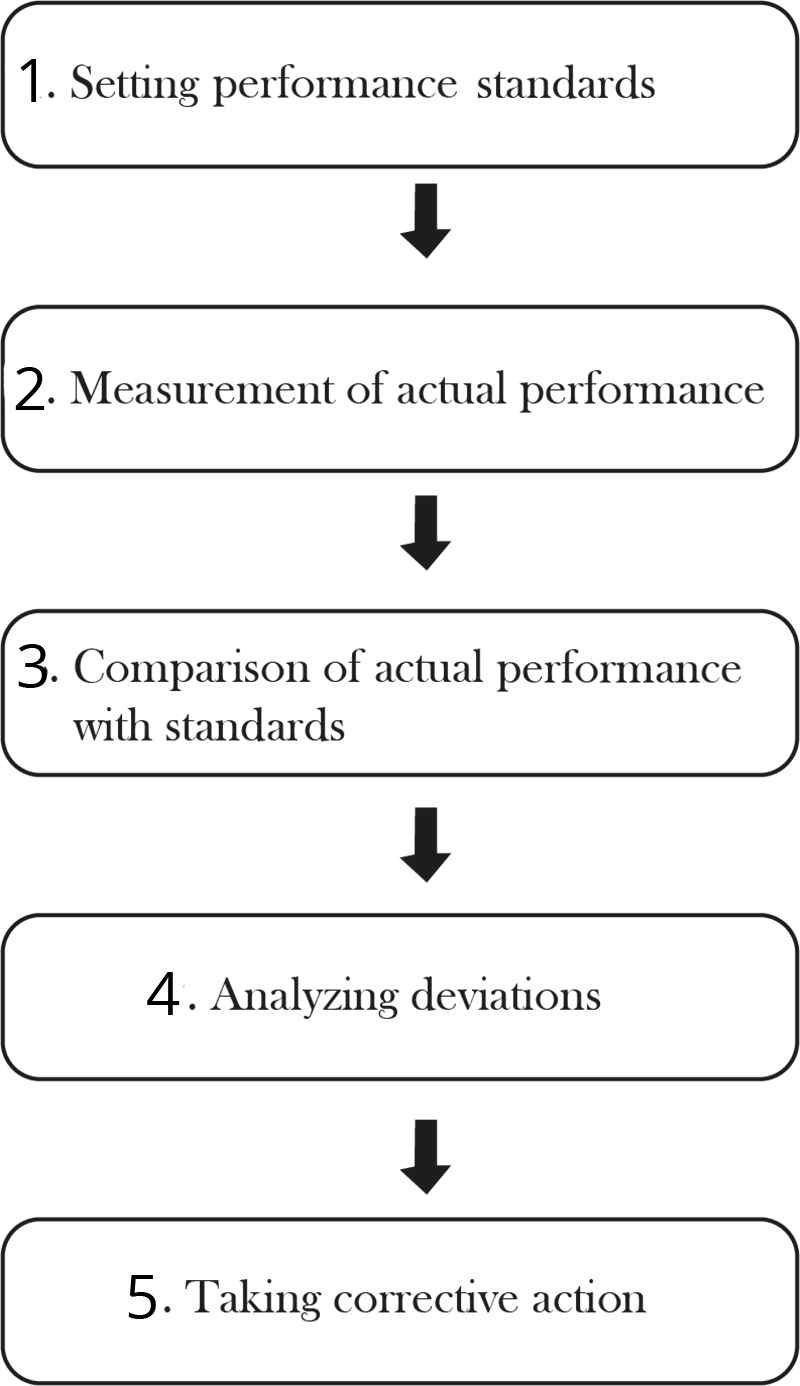

Controlling Process

1. Setting Performance Standards

Standards are criteria used to measure actual performance and reflect organisational goals.

They should be flexible to adjust to changes in the business environment.

Standards can be qualitative, quantitative, time-bound, or cost-bound.

2. Measurement of Actual Performance

Performance standards are first established, then actual performance is measured.

Use personal observation and sample checking for objective and reliable measurement.

Measure performance in the same terms as the standards to facilitate comparison.

Performance can be checked during or after the completion of the work.

3. Comparing Actual Performance with Standard

Compare actual performance to the established standards.

Three possible scenarios:

Standards = Actual Performance

Standards > Actual Performance

Standards < Actual Performance

4. Analysing Deviations

Determine permissible ranges of variation by assessing deviations from standards.

Critical Point Control: Focus on key result areas (KRAs) crucial to success.

Management by Exception: Focuses on significant deviations. for example, corrective action is taken when expenses exceed $10,000 or 20% of the budget.

5. Taking Corrective Action

Implement remedial actions if deviations exceed acceptable bounds.

No action is needed if variances are within acceptable limits.

Corrective actions address significant deviations to align performance with standards.

Important Topics of Business Studies Class 12 Chapter 8 Controlling

Learnings of Class 12 Chapter 8 of Business Studies

Understanding the Concept of Controlling

Importance and Role of Controlling in Management

Process of Controlling: Setting Standards, Measuring Performance, and Correcting Deviations

Benefits of Effective Controlling

Limitations and Challenges of Controlling

Importance of Revision Notes for Class 12 (Business Studies) Chapter 8 Controlling

Summarises Key Points: Condenses important concepts for quick review.

Saves Time: Provides a fast way to revise before exams.

Highlights Essentials: Focuses on crucial topics and definitions.

Improves Memory: Helps in better retention of information.

Enhances Exam Prep: Targets weak areas for more effective study.

Clarifies Concepts: Simplifies complex ideas for easier understanding.

Includes Visuals: Uses diagrams and charts for better grasp.

Boosts Confidence: Prepares students thoroughly for exams.

Tips for Learning the BST Class 12 Chapter 8

Focus on core processes with illustrations and examples.

Draw and label diagrams for clarity.

Create summaries of each process.

Connect concepts to everyday examples.

Solve past exam questions to test understanding.

Explain concepts to others to reinforce learning.

Revisit material frequently to retain information.

Utilise platforms like Vedantu for additional support.

Conclusion

Chapter 8 on Controlling underscores the essential role of controlling in management. It illustrates how effective controlling helps achieve organisational goals, optimises resource use, and enhances employee performance. However, it also addresses the challenges such as setting quantitative standards, dealing with external factors, and overcoming employee resistance. By understanding both the benefits and limitations, managers can better implement control systems to guide their organisations toward success.

Related Study Materials for Class 12 Chapter 8 Controlling

Revision Notes Links for Class 12 Business Studies

Important Study Materials for Class 12 Business Studies

FAQs on Controlling Class 12 Business Studies Chapter 8 CBSE Notes - 2026-27 Free PDF Download (Sign-in Required)

1. What are the main concepts highlighted in Controlling Class 12 Revision Notes for Business Studies?

The main concepts emphasised include the meaning of controlling, its importance in management, the controlling process (setting standards, measuring performance, correcting deviations), and the relationship between planning and controlling. The notes also discuss the features and limitations of controlling as per the CBSE 2026–27 syllabus.

2. How does the process of controlling ensure successful management in organisations?

Controlling ensures that actual performance is compared with set standards. When deviations are found, corrective actions are taken to align results with the goals. This continuous cycle helps achieve organisational objectives and maintains efficiency.

3. Why is controlling considered a continuous and forward-looking managerial function?

Controlling is continuous because it involves regular monitoring and assessment of performance at every stage. It is forward-looking because the insights gained help managers adjust future plans and strategies, ensuring ongoing improvement and goal achievement.

4. What are the limitations of the controlling function as discussed in Class 12 notes?

The main limitations include:

- Difficulty in setting quantitative standards for all areas

- Limited control over external factors like government policies and competition

- Resistance from employees to monitoring

- Expense of implementing control systems

5. What is the relationship between planning and controlling in business organisations?

Planning and controlling are interdependent functions. Planning sets the direction and standards, while controlling measures actual results against these plans. Effective controlling can highlight flaws in planning and lead to better future plans, making the two functions inseparable for successful management.

6. How can students use revision notes for Chapter 8 Controlling effectively before exams?

Students should focus on summarised key points, create concept maps for processes like steps in controlling, revisit important definitions, and use the notes for quick revision sessions. Frequent review aids in memory retention and builds exam confidence.

7. What are the critical features of the controlling function that help in achieving organisational goals?

The controlling function is goal-oriented, pervasive at all levels, continuous, action-oriented, and dependent on planning. By regularly tracking performance, it keeps everyone aligned with organisational objectives.

8. Why might employees resist the controlling process, and how can this challenge be managed?

Employees may resist controlling due to perceptions of strict monitoring or lack of trust. This can impact motivation and morale. To manage this, managers should communicate the purpose of controlling clearly, involve employees in goal-setting, and provide constructive feedback rather than criticism.

9. How does effective controlling contribute to efficient resource management?

By monitoring the use of resources against planned standards and taking corrective actions promptly, controlling helps minimise waste, optimise costs, and ensure that resources are allocated where they are most needed for organisational efficiency.

10. What changes should Class 12 students be aware of in the 2026–27 CBSE syllabus for the Controlling chapter?

As per the CBSE 2026–27 syllabus, the topic "Techniques of Controlling" has been deleted from Chapter 8. Students should revise only the prescribed topics and focus on the updated content for their exams.