How to Record and Amortize Preliminary Expenses in Final Accounts

Preliminary Expenses are the expenses incurred during the formation and establishment of a business or company before it starts its regular operations. These expenses are necessary for legally setting up the organization and ensuring that it is ready to commence business activities. In accounting, preliminary expenses are treated carefully because they are not part of the routine operational costs but relate to the initial setup of the enterprise.

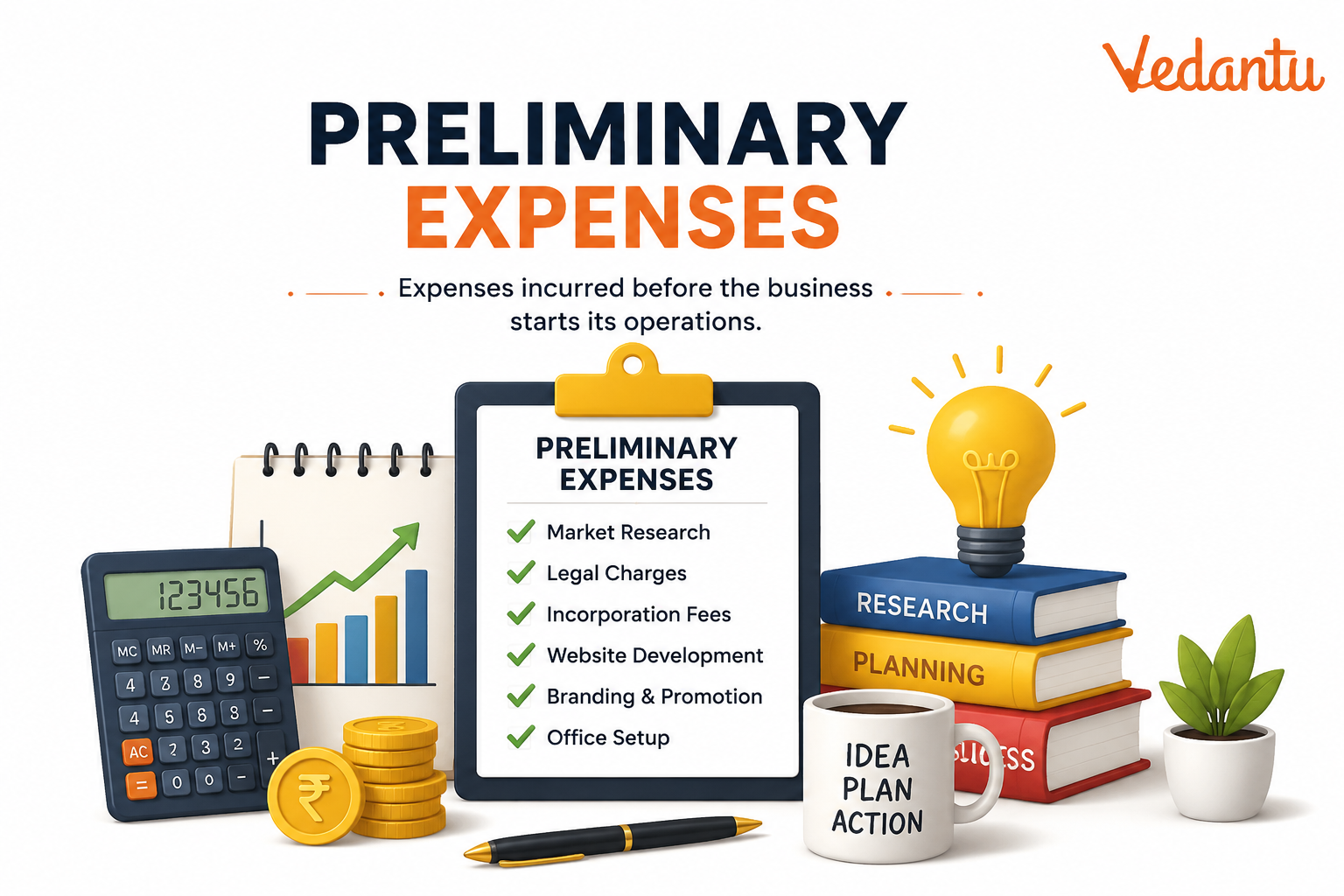

Meaning of Preliminary Expenses

Preliminary expenses refer to the costs incurred prior to the incorporation or commencement of business. These expenses are generally non-recurring in nature and are incurred only once at the time of formation of the company. They are also known as formation expenses or incorporation expenses.

These expenses are essential for legally registering and organizing the company, but they do not directly contribute to production or service activities.

Examples of Preliminary Expenses

Some common examples of preliminary expenses include:

- Legal charges for drafting Memorandum and Articles of Association

- Registration fees paid to the Registrar of Companies

- Stamp duty on legal documents

- Printing and stationery expenses for incorporation documents

- Professional fees paid to lawyers, accountants, or consultants for company formation

- Expenses related to the issue of prospectus

Features of Preliminary Expenses

- They are incurred before the commencement of business operations

- They are non-recurring in nature

- They are related to the formation and registration of a company

- They are capital in nature but do not create tangible assets

Accounting Treatment of Preliminary Expenses

In earlier accounting practices, preliminary expenses were shown as fictitious assets on the assets side of the Balance Sheet and written off over a period of time. However, as per modern accounting standards, these expenses should be written off in the year in which they are incurred.

This means that preliminary expenses are charged to the Profit and Loss Account and are not carried forward as assets unless specifically allowed under applicable accounting standards or laws.

Preliminary Expenses at a Glance

| Basis | Preliminary Expenses | Nature |

|---|---|---|

| Time of Occurrence | Before business starts | Pre-operational |

| Frequency | Incurred once | Non-recurring |

| Accounting Treatment | Written off to Profit and Loss Account | Expense |

The above table summarizes the essential aspects of preliminary expenses, including their timing, frequency, and accounting treatment. Understanding these basics helps students answer theoretical and practical questions in examinations.

Importance of Preliminary Expenses

Although preliminary expenses do not generate revenue directly, they play a crucial role in establishing the legal identity of a business. Without incurring these costs, a company cannot be properly registered or recognized under law.

- Ensure legal compliance during company formation

- Facilitate smooth commencement of operations

- Help in securing licenses and approvals

Difference Between Preliminary Expenses and Other Expenses

Preliminary Expenses vs Revenue Expenses

- Preliminary expenses are incurred before the start of business, while revenue expenses are incurred during normal business operations

- Preliminary expenses are one-time costs, whereas revenue expenses are recurring

- Revenue expenses are fully charged to the Profit and Loss Account in the same accounting period

Key Points for Students

- Preliminary expenses are also called formation expenses

- They are incurred before the business starts functioning

- They are non-recurring and usually written off in the year of occurrence

- They are important from an accounting and examination point of view

A clear understanding of preliminary expenses helps students grasp basic accounting concepts related to company formation and financial reporting. It is an important topic in school-level commerce, competitive exams, and introductory accounting studies.

FAQs on Preliminary Expenses in Accounting Explained Simply

1. What are Preliminary Expenses in accounting?

Preliminary Expenses are the expenses incurred during the formation of a company before it starts business operations. These are also known as pre-incorporation expenses or formation expenses.

- Legal charges for company registration

- Fees for drafting Memorandum and Articles of Association

- Stamp duty and registration fees

- Printing and documentation expenses

These expenses are initially treated as capital expenditure and later written off over a period as per accounting standards.

2. What are examples of Preliminary Expenses?

Examples of Preliminary Expenses include costs incurred before the commencement of business operations. Common examples are:

- Company incorporation fees

- Legal and professional charges

- Auditor’s fees for incorporation work

- Printing of prospectus

- Market survey expenses before formation

These expenses are related to company formation and not regular operating expenses.

3. Are Preliminary Expenses capital or revenue expenditure?

Preliminary Expenses are treated as capital expenditure because they are incurred to establish the business. However:

- They do not create a tangible asset

- They are shown under Miscellaneous Expenditure (if not written off)

- They are amortized over a few years as per accounting norms

Thus, they are capital in nature but gradually written off from profits.

4. How are Preliminary Expenses shown in the Balance Sheet?

Preliminary Expenses are shown on the assets side of the Balance Sheet until they are fully written off. They are usually recorded under:

- Other Non-Current Assets

- Miscellaneous Expenditure (if applicable)

After amortization, the remaining balance reduces each year until it becomes zero.

5. What is the treatment of Preliminary Expenses in accounting?

The accounting treatment of Preliminary Expenses involves amortization over time instead of charging them fully in one year. The steps include:

- Initially debited to a Preliminary Expenses account

- Shown as an asset in the Balance Sheet

- Written off gradually to the Profit and Loss Account

This ensures proper matching of expenses with future benefits.

6. Why are Preliminary Expenses written off?

Preliminary Expenses are written off to reflect true financial performance of a company. Reasons include:

- They do not provide long-term tangible benefits

- Accounting standards require systematic amortization

- To avoid overstating assets in the Balance Sheet

Writing them off ensures compliance with accounting principles and fair reporting.

7. What is amortization of Preliminary Expenses?

Amortization of Preliminary Expenses means spreading the total cost over several accounting periods. Key points include:

- A fixed portion is written off annually

- Charged to the Profit and Loss Account

- Reduces the balance shown in assets each year

This method follows the matching concept of accounting.

8. Are Preliminary Expenses allowed under Income Tax?

Preliminary Expenses are allowed as deductions under Section 35D of the Income Tax Act, subject to certain limits. Important conditions:

- Deduction is allowed over 5 years

- Applicable to specified formation expenses

- Subject to prescribed percentage of project cost

This provision benefits newly established businesses and companies.

9. What is the difference between Preliminary Expenses and Prepaid Expenses?

Preliminary Expenses and Prepaid Expenses differ in nature and purpose. The main differences are:

- Preliminary Expenses: Incurred before business commencement

- Prepaid Expenses: Paid in advance for future services

- Preliminary expenses are capitalized and amortized

- Prepaid expenses are current assets adjusted within a year

Thus, they serve different accounting functions.

10. When are Preliminary Expenses incurred?

Preliminary Expenses are incurred before the company starts its business operations. They arise during:

- Company formation stage

- Legal registration process

- Preparation of incorporation documents

- Raising initial capital

These expenses occur prior to revenue generation and are essential for business establishment.