How a Sinking Fund Works for Debt Repayment and Asset Replacement

A Sinking Fund is a financial strategy used by individuals, companies, and governments to set aside money regularly for a specific future purpose. The main objective of a sinking fund is to accumulate funds over time to repay debt, replace assets, or meet a large planned expense. Instead of facing a financial burden all at once, a sinking fund spreads the cost over a period, making financial management more systematic and disciplined. It plays a vital role in budgeting, financial planning, and long term stability.

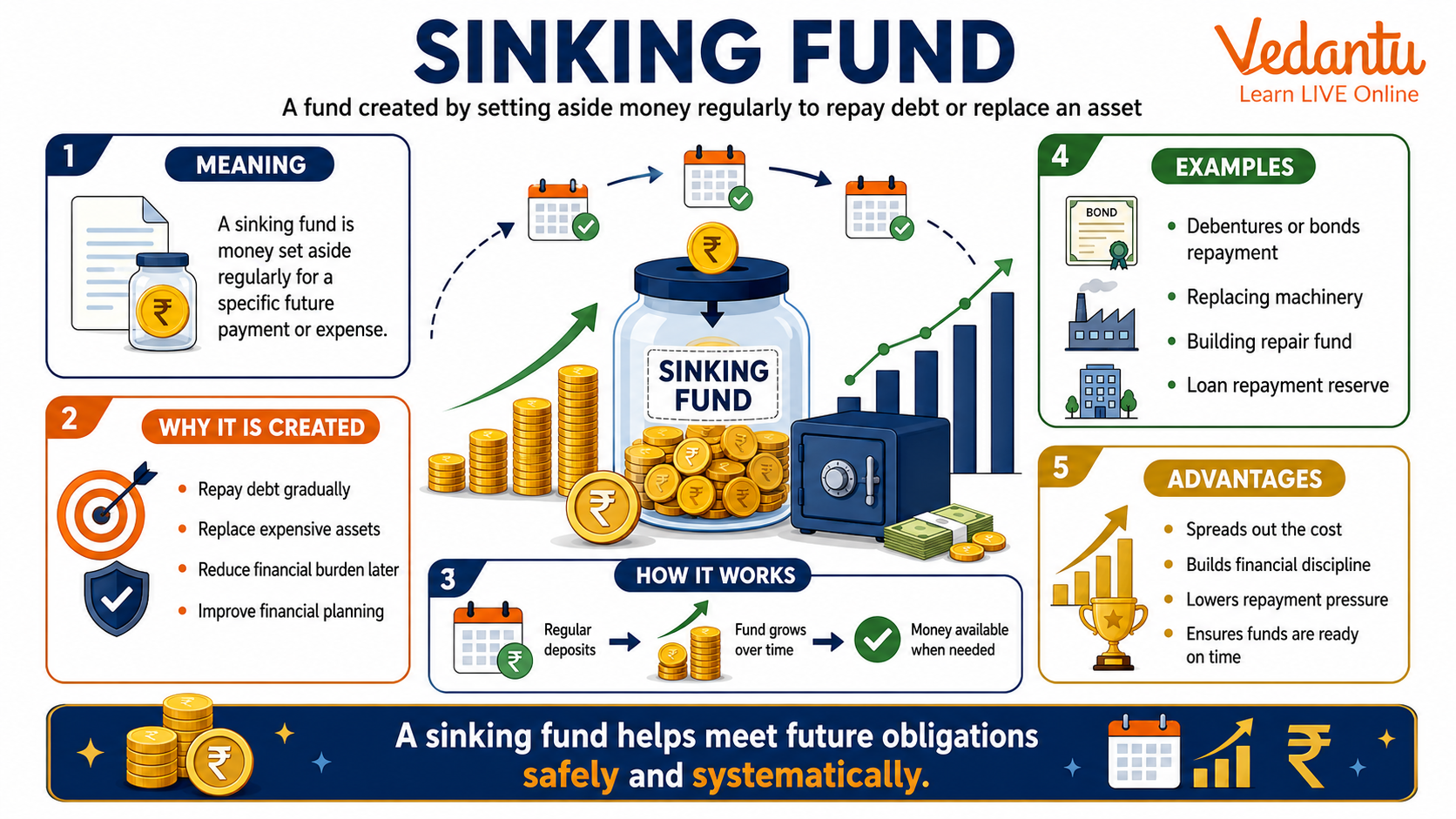

Meaning of Sinking Fund

A sinking fund is a reserve fund created by setting aside a fixed amount of money periodically to repay a debt or meet a future financial obligation. The term is commonly used in accounting, corporate finance, and public finance. The accumulated amount is often invested so that it earns interest, helping the fund grow faster.

Purpose of a Sinking Fund

The primary purpose of a sinking fund is to reduce financial risk and ensure that funds are available when required. It prevents sudden financial strain and promotes disciplined saving.

- Repayment of bonds or debentures at maturity

- Replacement of assets such as machinery or equipment

- Redemption of loans

- Meeting long term financial commitments

Features of a Sinking Fund

- Regular contributions are made at fixed intervals

- The fund is usually invested to earn interest

- It is created for a specific purpose

- Reduces default risk for lenders

- Ensures financial discipline and planning

How a Sinking Fund Works

The working of a sinking fund involves periodic deposits and accumulation with interest. The organization or individual calculates the total amount needed in the future and determines how much should be set aside regularly.

- Determine the total future liability

- Fix the time period for repayment

- Decide the rate of interest expected from investment

- Calculate the periodic contribution required

- Invest the amount regularly until maturity

Sinking Fund vs Other Funds

| Basis | Sinking Fund | Emergency Fund |

|---|---|---|

| Purpose | Planned future expense | Unexpected expenses |

| Time Frame | Long term | Immediate need |

| Planning | Pre determined | Uncertain events |

The sinking fund is created for a specific and planned objective, while an emergency fund is meant for unforeseen situations such as medical emergencies or sudden repairs. Both are important in financial management but serve different purposes.

Advantages of a Sinking Fund

- Reduces financial burden at maturity

- Improves creditworthiness of companies

- Encourages systematic saving

- Helps avoid sudden borrowing

- Provides financial security

Disadvantages of a Sinking Fund

- Requires regular allocation of funds

- May reduce available working capital

- Investment returns may fluctuate

Examples of Sinking Fund

A company issues bonds worth 10,00,000 rupees repayable after 5 years. Instead of arranging the full amount at the end of 5 years, the company sets aside a fixed amount every year into a sinking fund. The amount is invested in safe securities so that it grows with interest. At maturity, the accumulated amount is used to repay the bondholders.

Similarly, a housing society may create a sinking fund to replace elevators or repair major infrastructure after a certain period. Members contribute regularly to ensure sufficient funds are available when needed.

Importance in Financial Planning

The concept of a sinking fund is important in both personal and corporate finance. It reduces dependency on last minute borrowing and ensures that financial goals are achieved smoothly. Governments also use sinking funds to repay public debt, which helps maintain economic stability and investor confidence.

Conclusion

A sinking fund is a practical and disciplined financial tool designed to meet future obligations without stress. By making regular contributions and investing wisely, individuals and organizations can manage large expenses efficiently. Understanding the concept of a sinking fund is essential for students of commerce, accounting, and finance, as it forms a fundamental part of financial management and long term planning.

FAQs on Sinking Fund: Meaning, Calculation and Uses

1. What is a Sinking Fund?

A Sinking Fund is a fund created by a company or government to gradually repay a debt or replace an asset over time.

- It involves setting aside a fixed amount regularly (monthly or annually).

- The amount is invested to earn interest or compound returns.

- It ensures repayment of debentures, bonds, or long-term loans.

- Also known as a debt repayment fund or redemption fund.

This concept is widely used in financial management, corporate accounting, and competitive exams.

2. Why is a Sinking Fund important?

A Sinking Fund is important because it helps organizations avoid financial burden at the time of debt maturity.

- Reduces risk of default on bonds and debentures.

- Promotes disciplined savings and investment.

- Improves creditworthiness and financial stability.

- Helps in planned replacement of assets.

It answers common queries like "Why create a sinking fund?" and "How do companies repay debt safely?"

3. How does a Sinking Fund work?

A Sinking Fund works by depositing equal periodic amounts that accumulate with compound interest until the target sum is reached.

- A fixed sum is deposited every year.

- The deposit earns compound interest.

- The total grows to equal the debt amount at maturity.

- Calculations are based on the Sinking Fund Formula.

This method is common in corporate finance and loan repayment planning.

4. What is the formula for calculating a Sinking Fund?

The Sinking Fund Formula calculates the periodic deposit required to accumulate a future sum.

- Formula: A = S × r / ((1 + r)^n − 1)

- A = Annual deposit

- S = Future sum (debt amount)

- r = Rate of interest

- n = Number of years

This formula is frequently asked in commerce exams, banking exams, and financial mathematics.

5. What is the difference between a Sinking Fund and an Emergency Fund?

A Sinking Fund is for planned expenses, while an Emergency Fund is for unexpected expenses.

- Sinking Fund: Used for planned debt repayment or asset replacement.

- Emergency Fund: Used for sudden financial crises.

- Sinking funds are goal-specific and time-bound.

- Emergency funds are flexible and precautionary savings.

This distinction is common in questions about personal finance and financial planning.

6. Who creates a Sinking Fund?

A Sinking Fund is created by companies, governments, or institutions to repay long-term liabilities.

- Corporations for debenture redemption.

- Governments for public debt repayment.

- Municipal bodies for infrastructure bonds.

- Individuals for planned financial goals.

It is a common feature in corporate accounting and public finance.

7. What are the advantages of a Sinking Fund?

The main advantages of a Sinking Fund include financial security and systematic debt repayment.

- Reduces financial pressure at maturity.

- Encourages regular savings.

- Earns additional income through interest.

- Enhances investor confidence.

These benefits are often highlighted in commerce textbooks and competitive exam preparation.

8. What are the disadvantages of a Sinking Fund?

A Sinking Fund may limit liquidity and require consistent financial discipline.

- Funds are locked for a specific purpose.

- Requires regular contributions.

- Opportunity cost of invested money.

- Returns depend on interest rates.

This is relevant in discussions about investment planning and financial strategy.

9. How is a Sinking Fund shown in accounting?

In accounting, a Sinking Fund appears as a reserve and related investment in the balance sheet.

- Shown under Long-term Liabilities or Reserves.

- Investments are recorded separately as assets.

- Interest earned is added to the fund.

- Used specifically for debenture redemption.

This accounting treatment is important in financial statements and board exams.

10. Is a Sinking Fund compulsory for companies?

A Sinking Fund is not always compulsory but may be required by bond agreements or regulations.

- Often mandated in bond indenture agreements.

- Depends on company policy and legal provisions.

- Required in some government debt structures.

- Protects investors by ensuring repayment.

This question is common in corporate law, company accounts, and finance-related exams.