How Microfinance Institutions Support Rural and Small Business Borrowers in India

Microfinance Institutions India play a crucial role in promoting financial inclusion by providing small loans and financial services to low-income individuals who lack access to traditional banking facilities. These institutions focus on economically weaker sections, especially women, rural households, small entrepreneurs, and self-help groups. Microfinance Institutions India contribute significantly to poverty reduction, women empowerment, and rural development. This topic is important for competitive exams as it connects with banking, economy, government schemes, and financial inclusion initiatives in India.

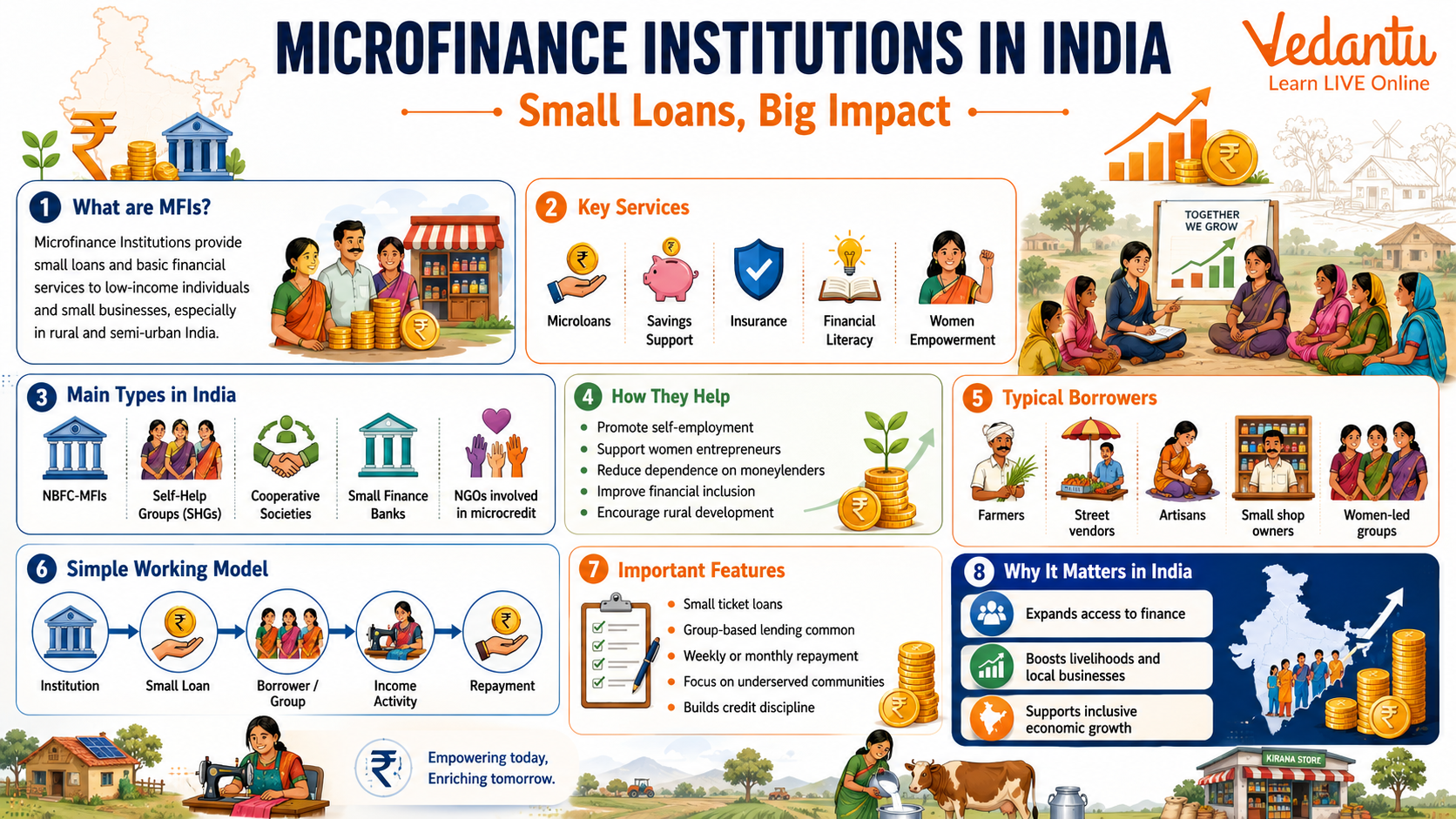

What are Microfinance Institutions India?

Microfinance Institutions India are organizations that provide financial services such as small loans, savings, insurance, and money transfer facilities to low-income individuals or groups who do not have access to formal banking services. The main objective is to promote self-employment and income generation activities among the poor.

- Provide small loans known as microcredit

- Focus on rural and semi-urban areas

- Encourage group lending models such as Self Help Groups

- Promote financial literacy and entrepreneurship

Objectives of Microfinance Institutions India

- Reduce poverty and unemployment

- Promote women empowerment through credit access

- Support small scale industries and rural enterprises

- Increase financial inclusion in remote areas

- Encourage savings habits among low income households

Types of Microfinance Institutions India

Types of Microfinance Institutions in India

| Type | Regulated By | Key Features |

|---|---|---|

| NBFC-MFI | Reserve Bank of India | Provide micro loans with specific lending norms |

| Self Help Groups | NABARD Support | Group based savings and lending model |

| Cooperative Societies | State Governments | Member owned financial services |

NBFC-MFIs are Non Banking Financial Companies registered with the Reserve Bank of India and follow specific microfinance guidelines. Self Help Groups operate under the SHG Bank linkage program supported by NABARD. Cooperative societies function at the local level and are owned by members who benefit from financial services.

Role of RBI in Microfinance Institutions India

The Reserve Bank of India regulates NBFC-MFIs and ensures transparency, fair lending practices, and borrower protection. RBI issues guidelines regarding interest rates, income criteria of borrowers, and repayment norms.

- Defines qualifying assets for microfinance

- Ensures borrower protection through fair practices code

- Monitors lending limits and repayment structures

- Promotes responsible lending

SHG Bank Linkage Programme

The Self Help Group Bank Linkage Programme was launched by NABARD in 1992. It connects Self Help Groups with formal banking institutions. Members save regularly and become eligible for loans based on collective savings and credit history.

- Encourages group responsibility

- Reduces default risk

- Strengthens rural credit delivery

Benefits of Microfinance Institutions India

- Improves income generation opportunities

- Enhances women participation in economic activities

- Supports rural development

- Encourages financial independence

- Promotes savings and credit discipline

Challenges Faced by Microfinance Institutions India

Despite their importance, Microfinance Institutions India face several operational and financial challenges.

- High operational costs in remote areas

- Risk of loan defaults

- Over borrowing by clients

- Regulatory compliance burden

- Limited financial literacy among borrowers

Importance for Competitive Exams

Microfinance Institutions India are frequently asked in exams related to banking, economy, and general studies. Questions may focus on SHG Bank linkage programme, role of RBI, types of MFIs, and objectives of financial inclusion. Understanding this topic helps in answering questions related to poverty alleviation, rural development, and government financial schemes.

Conclusion

Microfinance Institutions India serve as a powerful tool for financial inclusion and socio-economic development. By providing small loans and financial services to underserved populations, they help reduce poverty, empower women, and strengthen rural economies. Proper regulation by RBI and support from institutions like NABARD ensure that the microfinance sector operates responsibly and effectively. For students and competitive exam aspirants, this topic holds high relevance in understanding India’s inclusive growth strategy.

FAQs on Microfinance Institutions in India – Meaning, Role and Structure

1. What are Microfinance Institutions (MFIs) in India?

Microfinance Institutions (MFIs) in India are financial organizations that provide small loans and basic financial services to low-income individuals and self-employed groups who lack access to traditional banking.

- Microloans for small businesses and self-employment

- Micro-savings, insurance, and financial literacy services

- Focus on financial inclusion and poverty reduction

- Regulated mainly by the Reserve Bank of India (RBI)

MFIs play a key role in promoting inclusive growth, rural development, and women empowerment in India.

2. What is the main objective of Microfinance Institutions in India?

The main objective of Microfinance Institutions in India is to promote financial inclusion by providing affordable credit to economically weaker sections.

- Reduce poverty and unemployment

- Support self-help groups (SHGs) and small entrepreneurs

- Encourage women-led enterprises

- Reduce dependence on local moneylenders

MFIs contribute to economic empowerment, livelihood generation, and rural financial development.

3. How are Microfinance Institutions regulated in India?

Microfinance Institutions in India are regulated by the Reserve Bank of India (RBI) under specific guidelines for NBFC-MFIs.

- Classified as NBFC-MFI (Non-Banking Financial Company – Microfinance Institution)

- Must follow RBI norms on interest rates and lending limits

- Subject to Microfinance Regulatory Framework (2022)

- Monitored for fair practices and borrower protection

This regulation ensures transparency, borrower safety, and stability in the microfinance sector.

4. What is the difference between MFIs and banks in India?

The key difference between MFIs and banks lies in their target customers and scale of operations.

- MFIs provide small-ticket loans to low-income groups

- Banks offer a wide range of financial products to all income levels

- MFIs focus on group lending models and rural outreach

- Banks operate under stricter capital and regulatory norms

While banks promote general banking services, MFIs specifically target financially excluded populations.

5. What is the role of Self-Help Groups (SHGs) in microfinance?

Self-Help Groups (SHGs) are small groups of individuals, mainly women, who pool savings and access microloans collectively.

- Promote group lending and shared responsibility

- Linked to banks under the SHG-Bank Linkage Programme

- Encourage savings habits and financial discipline

- Enhance women empowerment and social development

SHGs are a cornerstone of India’s microfinance movement and rural credit system.

6. What are the types of Microfinance Institutions in India?

Microfinance Institutions in India operate under different legal structures to provide financial services.

- NBFC-MFIs regulated by RBI

- Self-Help Groups (SHGs)

- Non-Governmental Organizations (NGOs)

- Cooperative Societies

- Small Finance Banks (SFBs)

These diverse structures strengthen the microfinance ecosystem and expand rural banking access.

7. What is the SHG-Bank Linkage Programme?

The SHG-Bank Linkage Programme is a financial inclusion initiative launched by NABARD in 1992 to connect Self-Help Groups with banks.

- Provides bank credit to SHGs without collateral

- Encourages savings-led credit models

- Supports rural and women entrepreneurs

- One of the world’s largest microfinance programs

This programme strengthened India’s rural credit delivery system and grassroots financial empowerment.

8. What are the benefits of microfinance in India?

Microfinance in India helps improve livelihoods by offering easy access to small loans and financial services.

- Promotes entrepreneurship and self-employment

- Reduces poverty and income inequality

- Empowers women financially

- Supports rural and semi-urban development

Overall, microfinance drives socio-economic development and inclusive economic growth.

9. What challenges do Microfinance Institutions face in India?

Microfinance Institutions in India face operational and regulatory challenges despite rapid growth.

- High default and repayment risks

- Over-indebtedness of borrowers

- Regulatory compliance issues

- Limited financial literacy among clients

Addressing these issues is essential for sustainable growth of the Indian microfinance sector.

10. How do Microfinance Institutions contribute to women empowerment in India?

Microfinance Institutions significantly empower women by providing access to credit and income-generating opportunities.

- Majority of borrowers are women

- Support for women-led enterprises

- Increased household decision-making power

- Improved education and healthcare outcomes

By strengthening financial independence, MFIs promote gender equality and inclusive development in India.