Key Differences Between RuPay Card, Visa Card and MasterCard in India

Rupay Card, Visa Card, and Master Card are three major payment card networks used for digital transactions in India and across the world. These cards allow users to make payments online, withdraw cash from ATMs, and complete purchases at stores. While they perform similar functions, there are important differences in terms of origin, global acceptance, transaction cost, and network structure. Understanding the difference between Rupay Card, Visa Card, and Master Card is important for students, competitive exam aspirants, and general users who want to choose the right card for their financial needs.

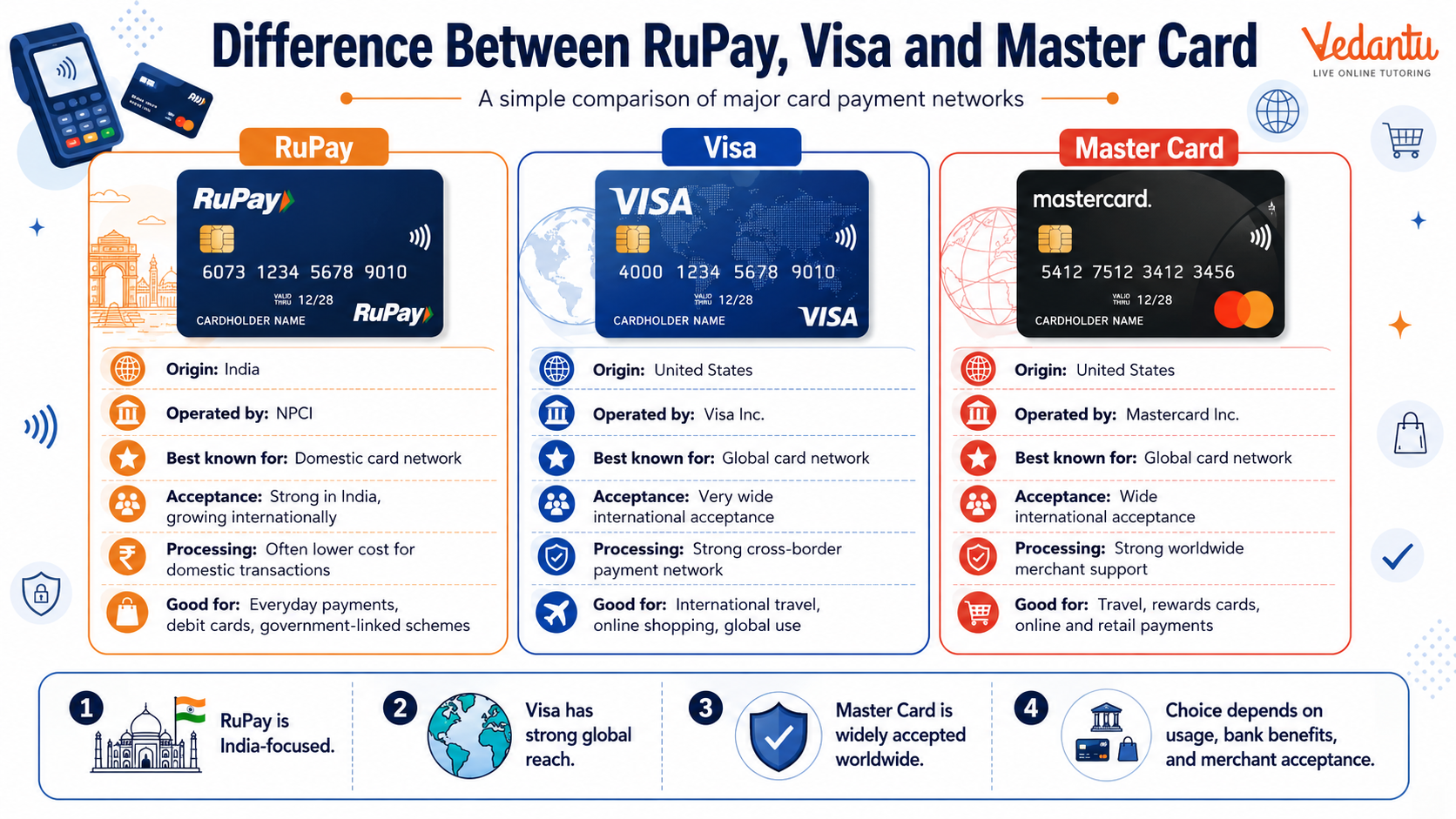

What is a Rupay Card?

Rupay Card is an Indian domestic card payment network launched by the National Payments Corporation of India - NPCI in 2012. It was introduced to reduce dependency on foreign payment networks and promote digital transactions within India. Rupay cards are widely used for debit, credit, and prepaid services and are especially popular under government schemes like Jan Dhan Yojana.

Key Features of Rupay Card

- Developed and operated in India by NPCI

- Lower transaction processing cost compared to international networks

- Widely accepted across India

- Linked with government benefit schemes

- Offers accidental insurance benefits on select cards

What is a Visa Card?

Visa is an international payment network headquartered in the United States. It is one of the largest global card networks and operates in more than 200 countries. Visa cards are issued by banks and financial institutions and are accepted almost everywhere in the world for online and offline transactions.

Key Features of Visa Card

- Global acceptance in over 200 countries

- High security standards with fraud protection

- Suitable for international transactions

- Offers reward programs and premium services

- Widely accepted for online shopping worldwide

What is a Master Card?

Master Card is another leading global payment network based in the United States. It operates in more than 210 countries and provides debit, credit, and prepaid card services. Like Visa, Master Card works through banks that issue cards to customers for domestic and international use.

Key Features of Master Card

- International acceptance across 210 plus countries

- Advanced security technologies for safe transactions

- Global ATM network access

- Reward programs and travel benefits on select cards

- Strong presence in both developed and developing countries

Difference Between Rupay Card, Visa Card, and Master Card

| Basis of Comparison | Rupay Card | Visa and Master Card |

|---|---|---|

| Origin | India - NPCI | United States |

| Global Acceptance | Mainly India with limited international support | Accepted worldwide in 200 plus countries |

| Transaction Cost | Lower processing cost | Higher processing cost |

| Usage | Best for domestic transactions | Best for international transactions |

| Government Support | Strong support under Indian schemes | No direct government scheme linkage in India |

The above table clearly shows that Rupay Card is primarily focused on domestic transactions in India, while Visa and Master Card are global networks suitable for international usage. The choice depends on the user's needs, such as domestic payments or international travel and shopping.

Advantages and Disadvantages

Advantages of Rupay Card

- Lower transaction fees for banks and merchants

- Supports financial inclusion in rural areas

- Integrated with Indian payment systems

Disadvantages of Rupay Card

- Limited international acceptance compared to Visa and Master Card

- Fewer global reward programs

Advantages of Visa and Master Card

- Wide global acceptance

- Strong international customer support

- Premium offers and travel benefits

Disadvantages of Visa and Master Card

- Higher transaction processing charges

- Dependent on international network infrastructure

Which Card Should You Choose?

The choice between Rupay Card, Visa Card, and Master Card depends on your financial needs. If you mainly perform domestic transactions within India and want lower charges, Rupay Card is suitable. If you frequently travel abroad, shop on international websites, or need global acceptance, Visa or Master Card is a better option. Many banks also provide dual network options, allowing customers to select based on convenience.

Conclusion

Rupay Card, Visa Card, and Master Card are important components of the digital payment ecosystem. Rupay represents India's effort toward financial independence and lower transaction costs, while Visa and Master Card dominate the global payment market with widespread acceptance and advanced services. Understanding their differences helps users make informed financial decisions and is also important from a General Knowledge and competitive exam perspective.

FAQs on Difference Between RuPay, Visa and MasterCard Cards Explained for Students

1. What is the main difference between RuPay, Visa, and MasterCard?

The main difference between RuPay, Visa, and MasterCard lies in their origin, network reach, and transaction processing systems.

• RuPay is an Indian domestic payment network launched by the National Payments Corporation of India (NPCI).

• Visa and MasterCard are global payment networks headquartered in the USA.

• RuPay has lower processing fees within India, while Visa and MasterCard offer wider international acceptance.

This difference between RuPay card and Visa card or MasterCard mainly affects global usability and transaction charges.

2. Which card is better: RuPay, Visa, or MasterCard?

The better card depends on your usage—domestic or international transactions.

• Choose RuPay card for lower transaction fees and government schemes like Jan Dhan Yojana.

• Choose Visa or MasterCard for global acceptance and international online payments.

• For frequent foreign travel, Visa and MasterCard are more widely accepted.

Thus, the comparison of RuPay vs Visa vs MasterCard depends on individual financial needs.

3. Is RuPay accepted internationally like Visa and MasterCard?

RuPay has limited international acceptance compared to Visa and MasterCard.

• Visa and MasterCard operate in over 200 countries worldwide.

• RuPay is mainly accepted in India but has expanded to countries like Singapore, UAE, Bhutan, and Nepal.

• International online merchants more commonly support Visa and MasterCard.

This makes Visa and MasterCard stronger global payment networks.

4. Why are RuPay cards cheaper than Visa and MasterCard?

RuPay cards are cheaper because they operate on a domestic payment network with lower processing costs.

• Managed by NPCI, reducing international transaction fees.

• Lower Merchant Discount Rate (MDR) compared to Visa and MasterCard.

• Promoted by the Indian government to encourage digital payments.

This cost advantage is a key difference between RuPay card and Visa card.

5. Who owns RuPay, Visa, and MasterCard?

RuPay, Visa, and MasterCard are owned by different organizations with distinct operational structures.

• RuPay is owned by the National Payments Corporation of India (NPCI).

• Visa Inc. owns and operates Visa globally.

• MasterCard Incorporated operates MasterCard worldwide.

This ownership difference explains why RuPay is India-focused while Visa and MasterCard are international brands.

6. Can I use a RuPay card for international online shopping?

You can use select RuPay cards internationally, but acceptance is limited compared to Visa and MasterCard.

• International usage depends on whether the RuPay card is enabled for global transactions.

• Many foreign websites prefer Visa or MasterCard.

• Check with your bank for international activation.

For seamless global e-commerce payments, Visa and MasterCard are generally preferred.

7. What are the similarities between RuPay, Visa, and MasterCard?

RuPay, Visa, and MasterCard function as payment processing networks that enable digital transactions.

• All allow ATM withdrawals, POS payments, and online transactions.

• Issued by banks as debit cards, credit cards, or prepaid cards.

• Provide security features like EMV chip and OTP authentication.

Despite operational differences, their core purpose is facilitating electronic payments.

8. Which card is more secure: RuPay, Visa, or MasterCard?

All three cards offer high security standards with advanced fraud protection systems.

• Use EMV chip technology for secure transactions.

• Provide two-factor authentication (2FA) and OTP verification.

• Follow global payment security standards like PCI-DSS.

Therefore, security differences between RuPay, Visa, and MasterCard are minimal.

9. Is RuPay card mandatory for government schemes in India?

RuPay cards are commonly issued under government financial inclusion schemes in India.

• Linked with Pradhan Mantri Jan Dhan Yojana (PMJDY).

• Offers built-in accident insurance cover.

• Encourages domestic digital payments.

This makes RuPay an important part of India’s financial inclusion initiatives.

10. What is the difference between RuPay debit card and Visa/MasterCard debit card?

The difference between RuPay debit card and Visa or MasterCard debit card lies in network coverage and transaction cost.

• RuPay debit card operates mainly within India with lower fees.

• Visa debit card and MasterCard debit card have global acceptance.

• International ATM and POS support is stronger for Visa and MasterCard.

Choosing the right debit card depends on whether you prioritize domestic savings or international convenience.