Breakdown of the 16-Digit Debit Card Number and What Each Digit Represents

The 16 digits printed on a debit card are not random numbers. Each digit has a specific meaning and plays an important role in identifying the card issuer, the bank, and the individual account holder. These numbers help in secure electronic transactions, ATM withdrawals, and online payments. Understanding what these 16 digits represent is useful for general knowledge, banking awareness, and competitive examinations.

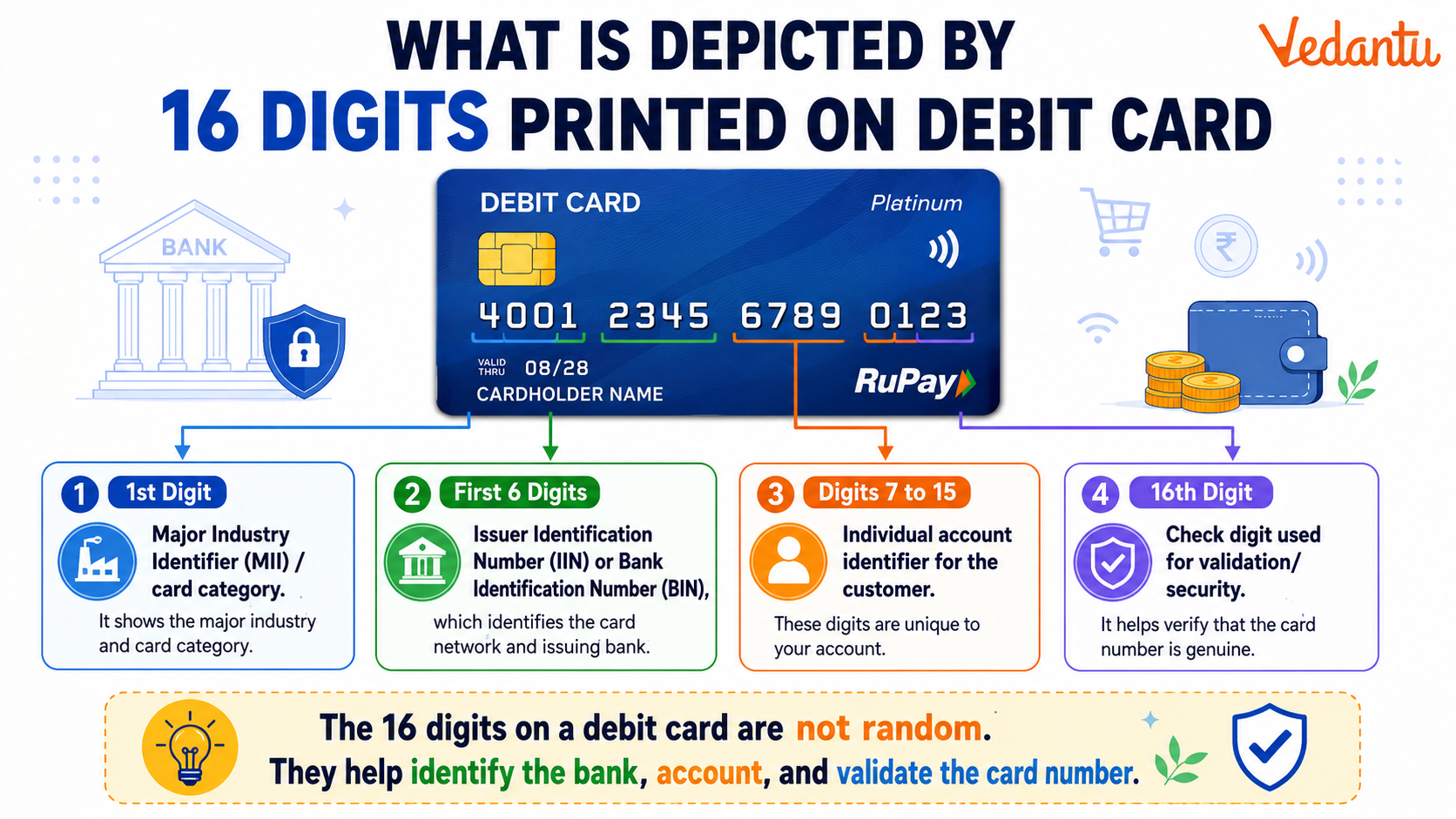

What Do the 16 Digits on a Debit Card Represent?

A standard debit card number usually contains 16 digits, divided into different sections. Each section provides specific information related to the card issuer and the customer account. The number is structured according to international banking standards set by the International Organization for Standardization.

Structure of 16 Digit Debit Card Number

| Digit Position | Name | Purpose |

|---|---|---|

| 1 | Major Industry Identifier | Identifies the card network |

| 2 to 6 | Issuer Identification Number | Identifies the issuing bank |

| 7 to 15 | Account Number | Identifies the cardholder account |

| 16 | Check Digit | Used for validation and security |

Each part of the 16 digit number works together to ensure accurate identification and secure processing of transactions across banking networks.

Detailed Explanation of Each Section

1. Major Industry Identifier - First Digit

The first digit of the debit card is known as the Major Industry Identifier. It shows the category of the card issuer. For example:

- 4 indicates Visa

- 5 indicates MasterCard

- 6 indicates Discover

This digit helps payment systems immediately recognize the card network.

2. Issuer Identification Number - First Six Digits

The first six digits together form the Issuer Identification Number. This number identifies the bank or financial institution that issued the debit card. Every bank has a unique Issuer Identification Number registered globally.

3. Account Number - Digits 7 to 15

Digits from the 7th to the 15th represent the unique account number of the cardholder. This part links the card directly to the customer bank account. It ensures that money is deducted from the correct account during transactions.

4. Check Digit - Last Digit

The 16th digit is called the check digit. It is generated using a mathematical formula known as the Luhn Algorithm. This digit helps verify whether the card number is valid or has been entered incorrectly during online or offline transactions.

Why Are These 16 Digits Important?

The 16 digit number plays a vital role in secure banking operations. Without this structured numbering system, global payment processing would not function efficiently.

- Ensures accurate identification of the issuing bank

- Helps in secure processing of online and offline payments

- Prevents transaction errors through validation digit

- Supports international payment systems

Security and Safety Measures

Although the 16 digit number is important, it should always be kept confidential. Fraudsters can misuse debit card information if proper safety measures are not followed.

- Never share your debit card number publicly

- Do not disclose CVV or PIN to anyone

- Use secure websites for online payments

- Regularly monitor bank statements

Difference Between Debit Card Number and Account Number

Many people confuse the debit card number with the bank account number. However, they are different. The debit card number is used for card based transactions, while the bank account number is used for direct banking transactions such as NEFT, RTGS, and deposits.

- Debit card number is 16 digits long

- Bank account number length varies by bank

- Debit card number is printed on the card

- Account number is mentioned in bank records and passbook

Conclusion

The 16 digits printed on a debit card are carefully structured to provide essential information about the card network, issuing bank, and cardholder account. Each digit has a specific role in ensuring secure and accurate financial transactions. Understanding this numbering system improves banking awareness and strengthens general knowledge, especially for students and competitive exam aspirants.

FAQs on What Is Depicted by the 16 Digits on a Debit Card? Meaning and Importance Explained

1. What do the 16 digits printed on a debit card represent?

The 16 digits on a debit card represent the unique card number used to identify the issuing bank and the cardholder’s account. These digits are structured as follows:

• First Digit (MII – Major Industry Identifier): Identifies the card network (e.g., 4 for Visa, 5 for Mastercard).

• First 6 Digits (IIN/BIN): Issuer Identification Number that identifies the bank or financial institution.

• Next 9 Digits: Unique account number of the cardholder.

• Last Digit: Luhn algorithm check digit used for validation and fraud detection.

This structure ensures secure electronic fund transfer and online transactions.

2. What is the meaning of the first digit on a debit card?

The first digit on a debit card is called the Major Industry Identifier (MII), which identifies the card network. Common examples include:

• 4 – Visa

• 5 – Mastercard

• 6 – Discover/RuPay

This digit helps determine the payment network and processing system used during card transactions.

3. What is the Issuer Identification Number (IIN) on a debit card?

The Issuer Identification Number (IIN), also known as the Bank Identification Number (BIN), consists of the first six digits of a debit card. It:

• Identifies the issuing bank

• Determines the card type (debit, credit, prepaid)

• Helps in transaction authorization and fraud prevention

This number is essential for routing payments through the correct banking network.

4. What does the last digit of a debit card number indicate?

The last digit of a debit card number is a check digit generated using the Luhn algorithm. It:

• Validates the card number format

• Detects typing errors during online payments

• Enhances transaction security

This digit does not represent bank details but ensures mathematical accuracy of the card number.

5. Why do debit cards usually have 16 digits?

Debit cards typically have 16 digits to provide a large number of unique combinations for global banking systems. This format:

• Supports millions of cardholders worldwide

• Ensures compatibility with ATM and POS machines

• Maintains standardized international payment systems

Some cards (like American Express) may have 15 digits, but 16 digits is the global standard.

6. Is the 16-digit debit card number the same as the bank account number?

No, the debit card number is different from the bank account number. Key differences include:

• Debit card number is used for card transactions.

• Bank account number is used for direct transfers (NEFT, RTGS, IMPS).

• The card number contains network and issuer information.

They are linked but serve different functions in the banking system.

7. How does the 16-digit number help in online transactions?

The 16-digit debit card number is essential for completing online payments and e-commerce transactions. It helps:

• Identify the card network and issuing bank

• Verify card validity through the Luhn check

• Process secure digital payments along with CVV and expiry date

Without this number, electronic payment gateways cannot authenticate transactions.

8. What security features are linked with the 16-digit debit card number?

The 16-digit debit card number works with several security features to prevent fraud. These include:

• CVV (Card Verification Value)

• Expiry date

• OTP (One-Time Password)

• PIN (Personal Identification Number)

Together, these elements ensure safe ATM withdrawals, POS payments, and online banking.

9. Can someone misuse the 16-digit number printed on a debit card?

Yes, the 16-digit debit card number can be misused if combined with other sensitive details. To prevent fraud:

• Never share your CVV or OTP

• Avoid saving card details on unsafe websites

• Enable transaction alerts via SMS/email

Protecting your card number ensures safety from cybercrime and financial fraud.

10. How are debit card numbers generated?

Debit card numbers are generated using standardized ISO/IEC 7812 banking guidelines. The process includes:

• Assigning a Major Industry Identifier (MII)

• Adding the bank’s Issuer Identification Number (IIN/BIN)

• Creating a unique account identifier

• Calculating the Luhn check digit

This structured generation ensures global compatibility in digital payment systems.