Key Differences Between Scheduled and Non-Scheduled Banks with Examples

Banks play a crucial role in the financial system of a country by accepting deposits and providing loans to individuals, businesses, and the government. In India, banks are broadly classified into Scheduled Banks and Non-scheduled Banks based on their inclusion in the Second Schedule of the Reserve Bank of India Act, 1934. Understanding the difference between Scheduled and Non-scheduled Banks is important for students, competitive exam aspirants, and general readers as it forms a fundamental part of banking and financial awareness.

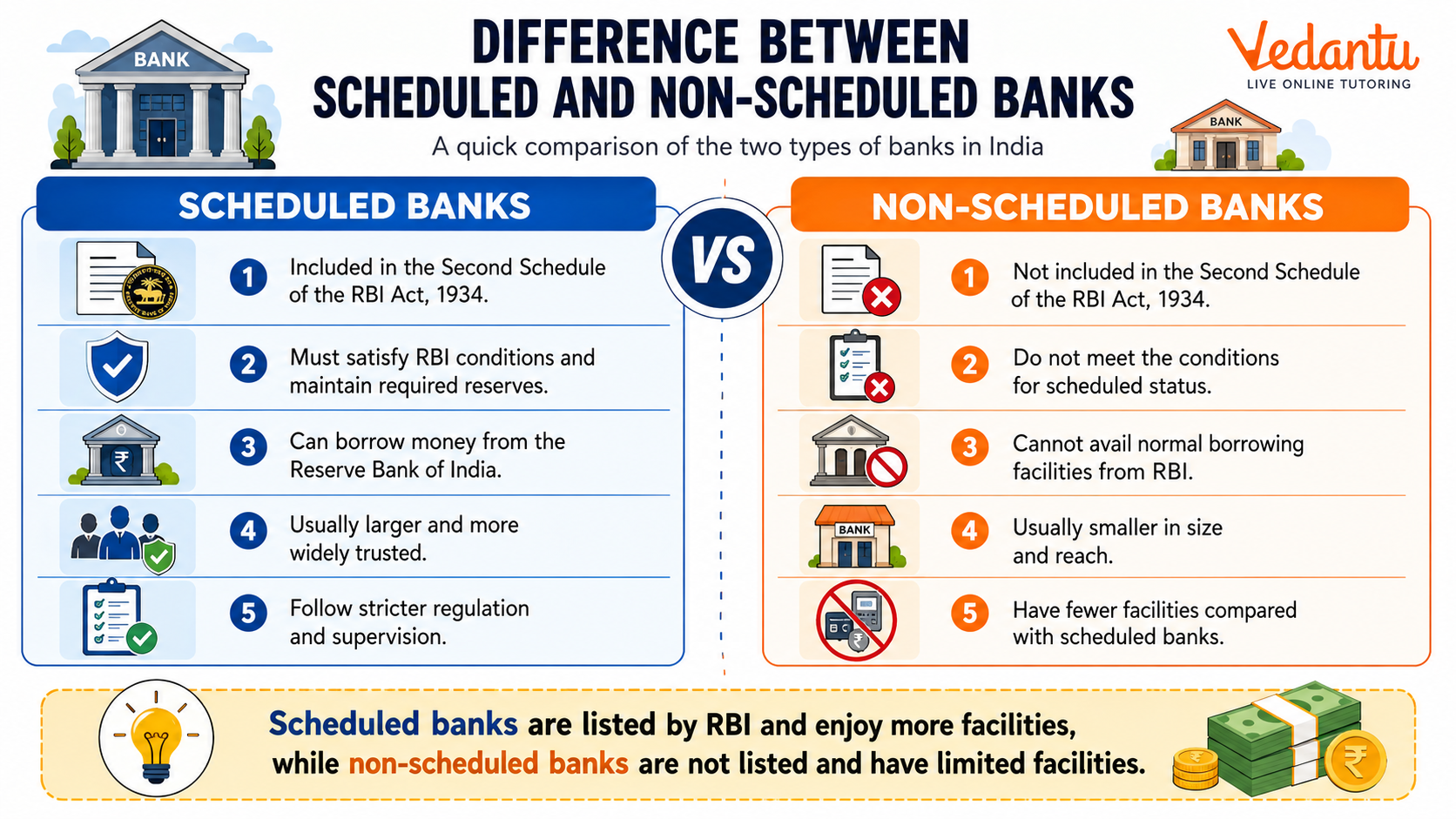

What Are Scheduled Banks?

Scheduled Banks are those banks that are listed in the Second Schedule of the Reserve Bank of India Act, 1934. These banks satisfy certain conditions laid down by the Reserve Bank of India (RBI), such as maintaining a minimum paid-up capital and reserves as prescribed by the RBI. Scheduled banks are entitled to certain facilities and privileges from the RBI.

Key Features of Scheduled Banks

- Included in the Second Schedule of the RBI Act, 1934.

- Must maintain a minimum paid-up capital and reserves as specified by RBI.

- Eligible for loans and financial assistance from RBI.

- Required to maintain Cash Reserve Ratio (CRR) with RBI.

- Considered more reliable and financially stable.

Examples of Scheduled Banks

- State Bank of India (SBI)

- Punjab National Bank (PNB)

- ICICI Bank

- HDFC Bank

- Axis Bank

What Are Non-scheduled Banks?

Non-scheduled Banks are those banks that are not listed in the Second Schedule of the RBI Act, 1934. These banks do not satisfy the conditions required for inclusion in the Schedule and generally operate on a smaller scale. They have limited access to RBI facilities and are subject to stricter regulatory monitoring.

Key Features of Non-scheduled Banks

- Not included in the Second Schedule of the RBI Act, 1934.

- Usually have lower paid-up capital and reserves.

- Not eligible for financial assistance from RBI in the same way as scheduled banks.

- Operate on a smaller scale and may have limited branches.

- Perceived as less stable compared to scheduled banks.

Difference Between Scheduled And Non-scheduled Banks

| Basis of Difference | Scheduled Banks | Non-scheduled Banks |

|---|---|---|

| Legal Status | Listed in Second Schedule of RBI Act, 1934 | Not listed in Second Schedule |

| Minimum Capital Requirement | Must meet RBI prescribed capital and reserve norms | May not meet RBI capital norms |

| RBI Assistance | Eligible for loans and support from RBI | Not entitled to regular RBI financial assistance |

| CRR Requirement | Required to maintain CRR with RBI | Also required but with limited facilities |

| Operational Scale | Operate on a large scale across regions | Operate on a smaller and limited scale |

The main difference between Scheduled and Non-scheduled Banks lies in their inclusion in the Second Schedule of the RBI Act and their eligibility for RBI facilities. Scheduled banks are more regulated, financially stronger, and widely trusted, while non-scheduled banks are smaller institutions with limited privileges.

Importance of Scheduled And Non-scheduled Banks in the Banking System

Both types of banks contribute to the financial structure of the country, although their scale and influence differ. Scheduled banks form the backbone of the Indian banking system, handling major financial transactions and government operations. Non-scheduled banks, though smaller, may serve local or specific community needs.

- Scheduled banks ensure financial stability and economic growth.

- They facilitate large scale credit creation and investment.

- Non-scheduled banks may cater to niche or regional markets.

- Together, they enhance financial inclusion.

Key Points for Competitive Exams

The difference between Scheduled and Non-scheduled Banks is frequently asked in banking awareness, general studies, and government job examinations. Students should focus on the legal basis, RBI facilities, capital requirements, and operational scale.

- Scheduled banks are listed in the Second Schedule of the RBI Act, 1934.

- They must maintain prescribed capital and reserves.

- They are eligible for RBI loans and clearing house facilities.

- Non-scheduled banks are not listed in the Second Schedule.

- Scheduled banks are generally more stable and widely recognized.

Conclusion

The difference between Scheduled and Non-scheduled Banks is primarily based on their registration under the RBI Act, 1934 and their compliance with capital requirements. Scheduled banks enjoy greater privileges, stronger regulatory oversight, and wider public trust. Non-scheduled banks operate on a smaller scale with limited benefits. A clear understanding of this classification helps students build strong fundamentals in banking and financial awareness.

FAQs on Difference Between Scheduled and Non-Scheduled Banks in India

1. What is the main difference between scheduled and non-scheduled banks?

The main difference between scheduled and non-scheduled banks lies in their inclusion under the Second Schedule of the Reserve Bank of India (RBI) Act, 1934.

• Scheduled Banks are listed in the Second Schedule of the RBI Act, 1934.

• Non-Scheduled Banks are not listed in this schedule.

• Scheduled banks must satisfy certain capital and reserve requirements.

• Non-scheduled banks have fewer regulatory privileges and facilities.

This distinction is important in banking exams, general knowledge, and understanding the Indian banking system.

2. What are scheduled banks in India?

Scheduled banks are banks included in the Second Schedule of the RBI Act, 1934 and regulated by the Reserve Bank of India.

• Must maintain a minimum paid-up capital and reserves as prescribed by RBI.

• Eligible to borrow money from the RBI at bank rate.

• Include public sector banks, private sector banks, foreign banks, regional rural banks, and cooperative banks.

• Subject to strict RBI supervision and compliance rules.

They form the backbone of the Indian banking structure.

3. What are non-scheduled banks?

Non-scheduled banks are banks not listed under the Second Schedule of the RBI Act, 1934.

• Do not meet the required minimum capital and reserve criteria.

• Cannot borrow funds from the Reserve Bank of India.

• Operate on a smaller scale compared to scheduled banks.

• Have limited banking privileges and fewer regulatory benefits.

These banks are less common and have minimal impact on the overall financial system.

4. What are the advantages of scheduled banks?

Scheduled banks enjoy several financial and regulatory benefits from the Reserve Bank of India.

• Eligible for RBI loans and refinance facilities.

• Greater public trust and credibility.

• Allowed to become members of the clearinghouse.

• Better liquidity support during financial crises.

These advantages strengthen their role in monetary policy and economic development.

5. What are the disadvantages of non-scheduled banks?

Non-scheduled banks face limitations due to restricted RBI support and lower financial strength.

• Cannot access RBI borrowing facilities.

• Limited operational area and customer base.

• Lower public confidence compared to scheduled banks.

• Not eligible for certain central banking privileges.

These drawbacks reduce their competitiveness in the Indian banking system.

6. Who regulates scheduled and non-scheduled banks in India?

Both scheduled and non-scheduled banks are regulated by the Reserve Bank of India (RBI).

• Scheduled banks are directly monitored under stricter RBI guidelines.

• Non-scheduled banks are also regulated but with fewer facilities.

• RBI ensures compliance with the Banking Regulation Act, 1949.

This regulation ensures financial stability and protection of depositors.

7. What are the types of scheduled banks in India?

Scheduled banks in India are classified into several categories based on ownership and function.

• Public Sector Banks (e.g., SBI, PNB).

• Private Sector Banks (e.g., HDFC Bank, ICICI Bank).

• Foreign Banks operating in India.

• Regional Rural Banks (RRBs).

• Scheduled Cooperative Banks.

This classification is important for competitive exams and banking awareness.

8. Why is inclusion in the Second Schedule of the RBI Act important?

Inclusion in the Second Schedule signifies financial stability and eligibility for RBI support.

• Ensures compliance with capital adequacy norms.

• Provides access to RBI credit facilities.

• Enhances trust among depositors and investors.

• Strengthens the bank’s position in the financial market.

Thus, scheduled status reflects reliability and regulatory approval.

9. Can a non-scheduled bank become a scheduled bank?

Yes, a non-scheduled bank can become a scheduled bank if it fulfills RBI requirements.

• Must meet the prescribed minimum paid-up capital and reserves.

• Should satisfy RBI’s regulatory and compliance standards.

• Must apply for inclusion in the Second Schedule of the RBI Act, 1934.

After approval, it gains scheduled bank status and related benefits.

10. Which is more secure: scheduled or non-scheduled banks?

Scheduled banks are generally considered more secure due to strict RBI regulation and financial backing.

• Regular supervision by the Reserve Bank of India.

• Access to emergency funds from RBI.

• Stronger capital structure and compliance norms.

• Higher public confidence and stability.

Therefore, scheduled banks are preferred for safety and reliability in the Indian banking system.