Accountancy Notes for Chapter 2 Theory Base of Accounting Class 11 - FREE PDF Download

Vedantu’s notes for Class 11 Accountancy Chapter 2 make learning the accounting basics easy. This chapter explains key ideas like the principles of accounting, which include important concepts such as the Going Concern Concept and Accrual Concept.

Table of Content

Table of ContentVedantu’s notes break down these ideas with simple explanations and examples, helping you understand them better. You can also download these notes for FREE as a PDF. These notes help you learn the chapter quickly and prepare well for your exams. By providing a summary and analysis, Vedantu makes it easier for students to see the lessons and ideas in the Class 11 Accountancy Revision Notes. Students can download the Theory Base of Accounting Class 11 Notes PDF, making it simple to study and review whenever they need with the updated CBSE Accountancy Class 11 Syllabus.

Accounting Principles

Accounting statements disclose the profitability and solvency of business to various parties. It is necessary to prepare such a statement in a standard language following a standard set of rules and regulations. These rules are known as “Generally Accepted Accounting Principles” or GAAP.

Features of Accounting Principles:

Accounting principles are man-made.

Accounting principles are generally accepted.

Accounting principles are flexible.

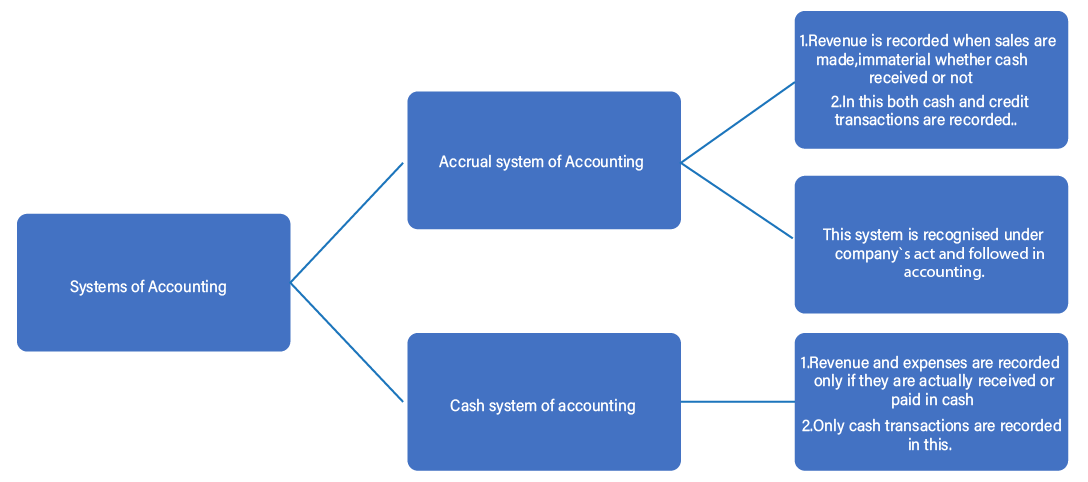

Systems of Accounting

Accounting Standards

Accounting standards are those written statements, which are issued from time to time by the accounting professional body, specifying uniform rules or practices for the preparation of the financial statements.

Need for Accounting Standards

Accounting standards are needed to improve reliability and bring uniformity in accounting practices and to ensure transparency, consistency, and comparability in financial information.

Benefits of Accounting Standards

Accounting standards make the financial statements more reliable.

Accounting standards help in resolving conflicts of financial interest among various groups.

Accounting standards ensure the consistency and comparability of financial statements.

Accounting standards significantly reduce the chances of manipulations and fraud.

Note- Accounting standards are applicable everywhere except purely charitable organisations.

International Financial Reporting Standards (IFRS)

The term IFRS refers to financial reporting standards issued by the International Accounting Standards Board (IASB). To make financial statements more consistent and transparent they should comply with all the requirements of IFRS.

Need for IFRS

The need for IFRS arises from the following reasons-

Easy access to global capital markets.

Easy to make Comparisons.

Uniformity in financial reporting.

True and fair valuation of assets.

Difficult to commit fraud and manipulate accounts.

Goods and Service Tax (GST)

Goods and Services Tax is an indirect tax levied on the supply of goods and services with consideration in the course of furtherance of business. GST is built on the principle of One Nation one Tax. It is a comprehensive, multistage, destination-based tax. GST extends to the whole of India including Jammu & Kashmir.

Features of GST

It is a consumption-based tax.

The burden can be shifted in respect of GST.

Taxpayers do not receive a direct pinch while paying indirect taxes.

It is regressive and it promotes social welfare

It is levied on commodities and services.

Advantages of GST

Ease of doing business.

Reduce Tax Evasion.

The tax system becomes more clear, more systematic, and more foreseeable.

Decrease in the cost of goods, since tax on tax is eliminated in the GST regime.

Note: There are 3 taxes applicable under GST:

Central Goods and Services Tax (CGST)

State Goods and Services Tax (SGST)

Integrated Goods and Services Tax/ Union Territory Goods and Services Tax. (IGST/UTGST)

Important Points from Theory Base of Accounting

1. GAAP - Generally Accepted Accounting Principles

GAAP refers to the standard rule and procedure for carrying out accounting transactions and presenting financial statements in a manner acceptable to the industry. Generally, the Financial Accounting Standards Board devised GAAP to attain the goals of transparency and comparability of financial statements with the view to enabling comparability of financial data across various organisations.

2. Accounting Concepts

Accounting concepts make sure that the entity maintains consistency and coherency in bookkeeping or any other financial practice as they offer a structured framework. Thus, one finds uniformity and efficiency in maintaining the books of accounts in a manner such that proper financial analysis can be conducted. The management too gets a clear vision of the financial system under which an entity is performing.

3. Business Entity Concept

The Business Entity Concept stipulates that a business entity is an aspect that is distinct from the owner; therefore, any financial transaction must be separately recorded for the business and the owner. The Business Entity Concept is also referred to as the Economic Entity Concept and it discards the act of mixing the finances of the business with the personal finances, thus ensuring that financial records remain clear and workable.

4. Money Measurement Concept

The Money Measurement Concept only precedes to include all those transactions that are expressed in monetary events. This helps in the treasuring of records in monetary units, and the properties are shown to have a monetary value which helps the financial reporting to be carried out with satisfactory revenue.

5. Going Concern Concept

Going Concern Concept: It is assumed that according to the going concern concept, a business is going to exist indefinitely and is not going to liquidate in any near future or be forced to stop its operations immediately. This is quite an important principle while preparing financial statements representing the going concern nature of business, its capability of meeting the financial obligations, and perpetual demand for its product or services.

6. Consistency Concept

The Consistency Concept requires that accounting methods and practices be consistent from period to period. Knowing that the same rules on recognition are applied in past and subsequent reporting periods makes comparative analysis and decisions appropriate.

7. Accrual Concept

The Accrual Concept states that when revenues and expenses are earned and incurred, they should be accounted for irrespective of the instant at which cash is exchanged for it. This concept keeps the consistency aspect through the alignment of the revenues with the expenses incurred in that period.

8. Dual Aspect Concept

The Dual Aspect Concept, or Double Entry System, states that for every transaction, there have to be at least two accounts getting affected, for which corresponding debits and credits are to be entered. This takes care of keeping the required equality of the accounting equation and at the same time reflects the dual nature of any transaction.

9. Cost Concept

This principle dictates the writing off of assets at the exact cost for which they are acquired. This facilitates the maintenance of the pertinence and objectivity in the valuation of assets in the financial statements of an enterprise.

10. Accounting Period Concept

The Accounting Period Concept is an aspect that allows the bifurcation of financial performance into a selected period, usually a year, for reporting purposes. It means the business gets an opportunity to periodically evaluate its financial performance and state of affairs.

11. Matching Concept

The Matching Concept refers to matching revenues earned with the expenses incurred to earn the revenues in the same accounting period. This principle will establish the financial results of the business accurately for the said period.

12. Accruals Concept of Revenue Recognition

Revenue should be recognized in the periods in which it is earned when it is realised or when its receipt is assured. This ensures that revenue is not overstated and hence presented accurately in financial statements.

13. Objectivity Concept

The Objectivity Concept stipulates that financial transactions should be recorded on an objective evidence basis. Such a concept in financial accounting ensures the objectivity of data contained in financial reporting since the information used in making financial statements is reliable and verifiable.

14. Concept of Conservatism

The concept of Conservatism guides the recognition of expenses and liabilities as early as possible and the recognition of revenues to recognise revenues when they are certain. When employed, this concept prevents the overstatement of financial health.

15. Concept of Materiality

The Materiality Concept states that financial information should be disclosed if its omission or misstatement might influence the decisions of users of financial statements. This will ensure that all the significant information is reported.

16. Full Disclosure Concept

The Full Disclosure Concept provides that any relevant financial information should be disclosed in the financial statements. The users are assured by this principle of access to all the information they require to make informed decisions.

17. Historical Cost Concept

Historical Cost Concept The asset should be recorded at the cost of its purchase. This provides objective, tangible, and verifiable evidence for the valuation of the asset.

18. Fair Value Concept

The Fair Value Concept records the assets and liabilities at their current market value rather than the historical cost of acquisition. Under this principle, the financial position of the entity would be shown more correctly concerning the current scenario.

19. Realisation Concept

The Realisation Concept states that Revenue Recognition is revenue to be recorded only if it is realised or realisable. This principle is used to state that the financial statement must show actual revenue.

20. Periodicity Concept

The Periodicity Concept is the concept that requires financial performance for some periods. Like quarterly or annually. This concept allows businesses to be able to know and measure the performance and financial status of businesses.

21. Economic Entity Concept

This view is supported by the Economic Entity Concept or Business Entity Concept to maintain appropriate books of accounts for the business.

22. Entity Assumption Concept

Assumes that business is a separate legal entity from owners and others, therefore presenting proper financial reporting along with separation of transaction

23. Duality Concept

The Duality Concept represents the dual aspect of transactions, thereby each transaction has a debit aspect and an equivalent credit aspect, which retains the balance in the accounting records.

24. Going Concern Principle

The Going Concern Principle lays down that a business establishment shall remain operative in perpetuity; this affects the accounting value of the entity in the books of account.

25. Relevance Concept

The Relevance Concept uses relevant and timely information for any decisions.

26. Reliability Concept

The Reliability Concept is used to file financial information that is clear of any material misstatements and biases, and therefore a sound base for making decisions.

27. Consistency Principle

The Consistency Principle smoothes the accounting and accounting principles' application consistently throughout the time the business is alive. That is, the comparability of financial statements is ensured and compelling.

28. Comparability Concept

The Comparability Concept The Comparability Concept allows financial statements to be compared for different time frames and entities, thereby making financial information more useful.

29. Understandability Concept

The Understandability Concept, on the other hand, dictates or ensures that financial information is presented in such a way that is very clear and understandable to its users for effective decision-making.

30. Timeliness Concept

The Timeliness Concept represents the view that accounting information must be reported in time so that it can be relevant to the decision-making process.

31. Prudence Concept

It cautions against overstatement of revenues and assets as well as understatement of liabilities and expenses in financial reporting.

32. Integration Concept

The Integration Concept guarantees users that financial statements or accounting practices are integrated with other business processes and systems to guarantee reliability and effectiveness in report preparation.

5 Important Topics of Class 11 Accountancy Chapter 2 you shouldn’t Miss!

Importance of Class 11th Accounts Chapter 2 Notes

Accounting Principles class 11 notes condense large amounts of information into key points, making it easier to review and remember essential concepts without getting overwhelmed.

They help you focus on the most important topics and concepts, ensuring you cover all necessary material efficiently.

Instead of re-reading entire textbooks, class 11 accounts chapter 2 notes allow you to quickly revisit and reinforce your understanding of key concepts.

They provide a quick way to refresh your memory before exams, making last-minute revision more effective.

By summarising and organising information, class 11th accounts chapter 2 notes can help clarify difficult concepts and improve overall comprehension.

Tips for Learning the Class 11 Accountancy Chapter 2 Theory Base of Accounting

Focus on understanding the main principles such as the Going Concern Concept and Accrual Concept. These are the foundation of accounting and crucial for financial accuracy.

Break down complex topics into smaller, manageable parts. Use simple language to explain each concept to make them easier to understand.

Write concise summaries of key topics. These notes should highlight the main principles and concepts, making it easier to review and memorise important information.

Apply the concepts to practise questions and problems. This helps reinforce your understanding and prepares you for exam questions.

Schedule regular review sessions to go over your theory base of accounting class 11 notes PDF and key concepts. Frequent revision helps keep the material fresh in your mind.

Conclusion

In conclusion, Class 11 Accountancy Chapter 2 on the Theory Base of Accounting provides a fundamental understanding of key accounting principles and concepts. By understanding principles like the Going Concern Concept, Accrual Concept, and Consistency Concept, students gain the essential knowledge needed for accurate financial reporting and analysis. Understanding these concepts ensures a strong foundation for more advanced accounting topics and practical applications.

Related Study Materials for Class 11 Accountancy Chapter 2 Theory Base of Accounting

Revision Notes Links for Class 11 Accountancy

Important Study Materials for Class 11 Accountancy

FAQs on Theory Base of Accounting Class 11 Accountancy Chapter 2 CBSE Notes - 2026-27 Free PDF Download (Sign-in Required)

1. What is a quick summary of the key concepts in Class 11 Accountancy, Chapter 2, "Theory Base of Accounting"?

This chapter provides the foundational rules for accounting. For a quick recap, focus on: Generally Accepted Accounting Principles (GAAP), which are the common set of rules; the core Accounting Concepts like Business Entity and Going Concern; and the formal Accounting Standards (including IFRS) that ensure uniformity and comparability in financial statements.

2. For revision, what are the three fundamental accounting assumptions I must know from this chapter?

The three fundamental accounting assumptions you should remember are:

- Going Concern: The assumption that a business will continue its operations for the foreseeable future.

- Consistency: The principle that a company must use the same accounting methods from one period to the next to allow for fair comparison.

- Accrual: The concept of recording revenues and expenses when they are earned or incurred, not necessarily when cash is exchanged.

3. What is the main difference to remember between the 'Business Entity Concept' and the 'Money Measurement Concept'?

The key distinction for revision is:

- The Business Entity Concept states that the business is separate from its owner. All transactions are recorded from the business's viewpoint, not the owner's personal one.

- The Money Measurement Concept states that only transactions that can be expressed in monetary terms are recorded in the accounts. It provides a common unit for measurement.

4. How does the 'Matching Concept' ensure the accurate calculation of profit for a period?

The Matching Concept is crucial for accurate profit calculation because it dictates that all expenses incurred to earn revenue in a specific accounting period must be recorded in that same period. This prevents expenses from one period being incorrectly set against revenues of another, providing a true and fair view of profitability for that period.

5. Why is it necessary to follow a standard 'Theory Base of Accounting' like GAAP?

Following a standard theory base like GAAP (Generally Accepted Accounting Principles) is essential to ensure financial statements are reliable, consistent, and comparable. Without these common rules, every business could report its finances differently, making it impossible for investors, lenders, and management to compare performance or make informed decisions. It brings uniformity and credibility to financial reporting.

6. During revision, what is the best way to distinguish between Accounting Principles and Accounting Standards?

Think of it this way: Accounting Principles are the fundamental, general guidelines (like the 'Accrual Concept') that form the basis of accounting theory. Accounting Standards (like those issued by IASB or ICAI) are the specific, authoritative written rules that mandate how transactions should be treated and presented in financial statements. In short, Principles are the 'why,' and Standards are the 'how'.

7. How does the 'Conservatism' or 'Prudence' concept help in creating a reliable financial statement?

The Conservatism Concept, also known as Prudence, enhances reliability by ensuring that a business does not overstate its profits or assets. The guideline is to anticipate and record potential losses or liabilities as soon as they are foreseen, but only recognise revenues or gains when they are certain. This cautious approach provides a more realistic view of the company's financial health.

8. How do modern regulations like GST and IFRS connect to the core ideas in this chapter?

GST and IFRS are practical applications of the core concepts in the Theory Base of Accounting. IFRS (International Financial Reporting Standards) promotes the principles of comparability and transparency on a global scale. Similarly, GST ('One Nation, One Tax') implements the principle of uniformity in indirect taxation, simplifying the tax structure and ensuring consistency across the country.