What is Redemption of Debentures?

What is Debenture and Redemption of Debenture?

First, what is a debenture? a debenture is a form or structure designed for long-term debt or loans that corporations or firms use to accept to borrow money from the public. It is common for debentures to remain unsecured even when borrowers have pledged to repay the loan in full after the term has expired. In India, like in many other countries, the loan is often collateralised by the company's or firm's secured assets. In the United States, however, they are still not protected.

Debentures are redeemed when the holder settles all outstanding obligations and loans owed to the debenture holder or the lender that provided the loan. It includes the parties' agreed-upon terms and conditions for the loan or debt repayment.

The term "redemption of debentures" describes how a corporation pays back loaned money to its creditors after maturity. The obligation is cancelled when the debt on the debenture account is paid in full.

What Does DRR (Debenture Redemption Reserve) Mean?

Defining the Term Debenture Redemption Reserve

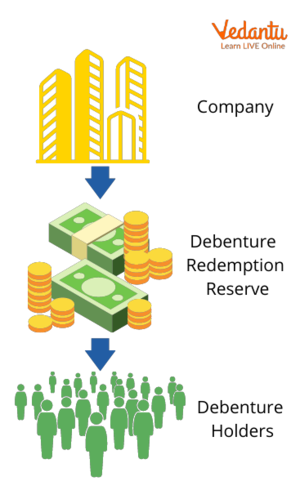

A debenture redemption Reserve is a clause stating that any corporation, firm, or organisation in the nation that issues debentures is needed to establish a redeeming service of the debenture to demonstrate an attempt to assure the return of borrowed money.

Companies that issue debentures in India must set aside funds for debenture redemption well before the debenture's maturity date, as required by the Indian Companies Act of 1956. To issue debentures under this Act, a company must have a minimum of 25 percent of the face value represented by the debentures.

For Example, On April 1, 2022, ABC Pvt Ltd. issued Rs. 20 lakhs in debentures with a maturity date of March 1, 2025. In this case, ABC Pvt. Ltd. is required by the Companies Act to set aside Rs. 5 lakhs (or 25% of the debenture's face value) as a debenture redemption reserve by the debenture's maturity date.

After issuing a debenture, companies are not obligated to immediately set aside money for the redemption reserve. Instead, they may put a sufficient sum into the DDR account each year until maturity.

Redemption Reserve Methods

Debentures can be redeemed in several different ways. For bookkeeping purposes, each approach is handled differently. It is possible to place these methods into the following buckets:

Lump-sum Method

After the maturity term, the corporation will make a single redemption payment in full to the holder of the debenture. The principal amount and maturity date will be agreed upon during debenture issuance. Since the corporation knows the maturity date, it can plan accordingly. In addition, this debenture amount received in lump sum includes the cash held in the debenture's redemption reserve account.

Instalment Method

In this form of debenture redemption, the borrowed funds are repaid in a series of payments, either regularly or irregularly, depending on the rescue of the debenture above.

Purchasing Method

Market participants are eager to buy the debentures these corporations and organisations issued. They may also be terminated instantly, allowing the corporation to extend the debenture's term until its repayment is within its means.

In addition, the corporation may increase its income by purchasing debentures on the open market at a discount, which reduces the total redemption payment.

Conversion Method

Conversion to a different debenture or stock in the issuing firm is an additional perk of redeemable debentures. As part of the debenture's issuing process, the holder is informed of the terms and circumstances under which the debenture may be converted.

Convertible debentures are the word used to describe this kind of debt instrument. At par, at a discount, or at a specified premium, the company can issue new equity shares in exchange for such debentures or issue new debentures.

A company can redeem its debentures by at least 15% of its face value during the investment year if the firm is investing in designated securities under Rule 18 (7) of the Companies Share Capital and Debenture Rules 2014. This must be completed by April 30 of the maturity year. Finally, businesses must remember that the DRR account may be established at any Indian bank recognised by the Reserve Bank of India.

Case Study

Show the example of Redemption of Debentures Journal Entries.

On March 31, 2002, X Co. Ltd. paid Rs. 97 for its own 9% debentures with a nominal value of Rs. 40,000. Input the transaction into the company's accounting system. If the price quoted is:

(i) Cum-interest

(ii) Ex-interest.

The company pays debtor interest twice a year, on June 30 and December 31.

Solution:

Conclusion

The functioning of debentures in an organisation is made possible by the procedures of issuing new debentures and redeeming existing ones. Therefore, discharging an organisation's debt burden of debentures is meant as "debenture redemption." One of the many methods for redeeming debentures is to make a one-time payment in the form of a lump amount. Other methods are also available. In this scenario, debenture holders get the guaranteed amount on the date that has been predetermined.

FAQs on Redemption of Debentures: Key Steps and Examples

1. What is the redemption of debentures?

Redemption of debentures is the process of repaying the principal amount to the debenture holders, thereby discharging the company's liability. This repayment is made at the end of a specified period (on maturity) or earlier, as per the terms of issue agreed upon when the debentures were first offered.

2. What are the main methods a company can use to redeem its debentures?

A company can redeem its debentures using several methods, as per the CBSE Class 12 Accountancy syllabus for 2025-26. The primary methods are:

- Lump-sum Payment: Repaying the entire amount to debenture holders on the maturity date.

- Payment in Instalments: Redeeming debentures in parts over specified intervals, often through a 'draw of lots'.

- Purchase in the Open Market: Buying back its own debentures from the stock exchange if they are available at a price lower than their redemption value.

- Conversion into Shares or New Debentures: Offering debenture holders the option to convert their holdings into equity shares or new debentures.

3. What is a Debenture Redemption Reserve (DRR) and is it always required?

A Debenture Redemption Reserve (DRR) is a special reserve created out of a company's profits available for dividend distribution. Its purpose is to safeguard the interests of debenture holders by ensuring funds are set aside for redemption. As per the Companies Act, 2013, and SEBI guidelines, a company must create a DRR equivalent to a certain percentage of the value of outstanding debentures before redemption begins. However, certain entities like All India Financial Institutions and Banking Companies are exempt from this requirement. You can learn more about the Debenture Redemption Reserve (DRR) and Debenture Redemption Investment on our detailed page.

4. How do you calculate the amount to be transferred to the Debenture Redemption Reserve (DRR)?

According to the Companies (Share Capital and Debentures) Rules, 2014, a company is required to create a Debenture Redemption Reserve (DRR) of at least 25% of the nominal (face) value of the debentures to be redeemed. This amount must be transferred from the company's profits before the redemption process starts. For example, if a company has to redeem debentures worth ₹10,00,000, it must have at least ₹2,50,000 in its DRR account.

5. What is the difference between redemption out of profits and redemption out of capital?

The key difference lies in the source of funds used for redemption.

- Redemption out of Profits: This means the company uses its accumulated profits to redeem debentures. It involves creating a full Debenture Redemption Reserve (DRR) equal to 100% of the value of the debentures being redeemed. This protects the company's capital structure.

- Redemption out of Capital: This implies that profits are not used, and the redemption is financed from other sources, including fresh capital. In this case, the company only needs to create the minimum legally required DRR (e.g., 25%). The rest of the funds can come from the company's capital sources.

6. Why would a company choose to purchase its own debentures from the open market?

A company might opt to purchase its own debentures from the open market for strategic financial reasons. The primary motives are:

- Immediate Cancellation: If the market price of the debentures is lower than their face value, the company can buy them back at a discount and make a profit on cancellation. This is a Capital Profit.

- Investment Purposes: The company can buy its debentures as an investment and sell them later at a higher price, earning a profit.

- Avoiding Interest Payments: By buying back its debentures, the company reduces its outstanding debt and saves on future interest payments.

7. What is the journal entry for redeeming debentures at a premium?

When debentures are redeemed at a premium (i.e., paying more than the face value), the premium is a capital loss for the company. The journal entry for making the amount due to debenture holders is:

Debentures A/c Dr. (with nominal/face value)

Premium on Redemption of Debentures A/c Dr. (with the premium amount)

To Debenture Holders A/c (with the total amount payable)

This entry records the liability towards the debenture holders at the redemption price. You can find more detailed examples in our NCERT Solutions for Class 12 Accountancy Chapter 2.

8. Can a company in India issue irredeemable debentures?

No, a company in India cannot issue irredeemable debentures, which are debentures with no fixed date of repayment. According to the Companies Act, 2013, all debentures must be redeemable. They must be redeemed within a specific period, which is generally a maximum of 10 years from the date of issue. For certain infrastructure companies, this period can be extended, but they cannot be perpetual or irredeemable.

9. What happens if a company fails to redeem its debentures on the due date?

If a company defaults on the redemption of its debentures, it is a serious breach of contract. The Debenture Trustee can take action on behalf of the debenture holders. They can file a suit against the company to recover the money. Furthermore, the National Company Law Tribunal (NCLT) can intervene and order the company to repay the principal amount along with any accrued interest immediately. This can severely damage the company's creditworthiness and reputation.