Master Introduction To Accounting Class 11 Questions And Answers For Better Exam Results

Class 11 Accountancy NCERT Solutions Chapter 1, Introduction to Accounting provides students with the fundamentals of business financial management. This chapter discusses proper transaction recording, preparing necessary financial statements such as the income statement and balance sheet, and recognising the importance of accounting in company decision-making.

Table of Content

Table of ContentIn Class 11 Accountancy Chapter 1 Question Answers are prepared by our Master Teachers and provide real-world scenarios and exercises that are used continuously to help students understand these necessary principles. Check out the revised Class 11 Accountancy syllabus and start practising Accountancy Class 11 Chapter 1.

1. Define accounting.

Ans: Accounting is a method of identifying the occasions of monetary nature and recording them in a magazine, classifying in their respective ledgers, summarizing them in earnings and Loss Account and Balance Sheet and providing the consequences to the users of such information, viz. owner/s, government, creditors, traders etc.

According to the American Institute of Certified Accountants, 1941, "Accounting is an art of recording, classifying and summarizing in a significant manner and in terms of money transactions and events that are, in part at least, of a financial character and interpreting the results thereof."

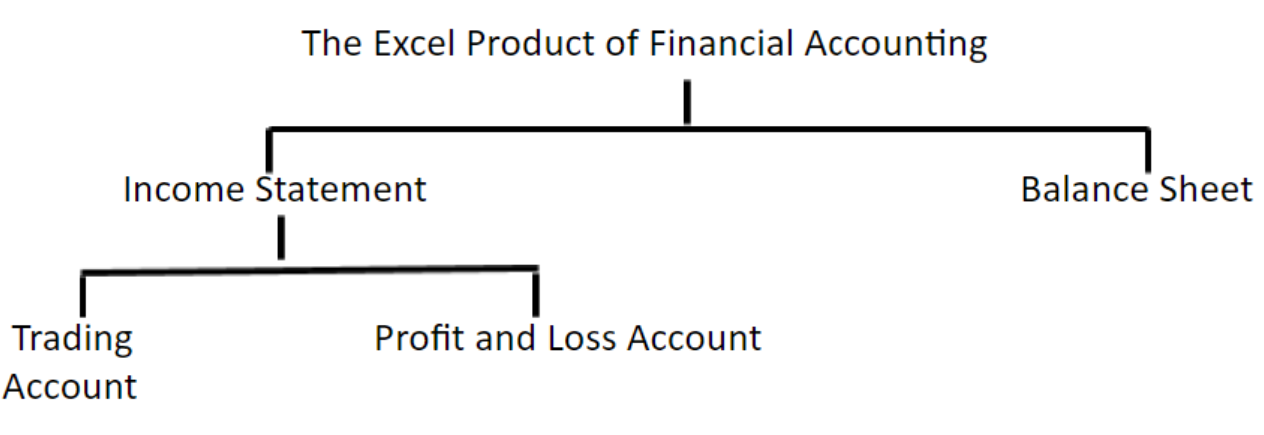

2. State what is the end product of financial accounting?

Ans:

1. Income statements (Trading and/or Profit and Loss Account) - An income statement that includes Trading and Profit and Loss Account, ascertains the financial results of a business in terms of gross (or net) profit or loss.

2. Balance Sheet - It indicates the real monetary positions of a commercial enterprise that gives required facts of and liabilities of an enterprise company, to folks that require information like owners, creditors, investors, authorities, and many others.

3. Enumerate the main objectives of accounting.

Ans: The primary objectives of accounting are given under

1. To preserve a systematic report of all transactions which occur.

2. To predict and calculate the income earned or loss incurred all through an accounting duration via getting ready income and loss accounts.

3. To expect the financial position of the enterprise at the cease of every accounting period by means of getting ready to balance sheets.

4. To assist the management for selection making, effective manipulation, forecasting, etc.

5. To forecast the destiny choices for the betterment of the business.

6. To come across and save you frauds and errors

7. To communicate statistics to diverse customers

4. Who are the users of accounting information?

Ans: Users customers of accounting records are divided into two classes as - inner customers and outside users.

1. Inner users

Inner customers are typically referred for the employees of the enterprise. They have a direct right of entry to the monetary statements of a commercial enterprise. Examples are given below.

i. Owners

ii. Management

iii. Personnel and people

2. External users

External customers are individuals who aren't an employee of the corporation and are inquisitive about the monetary affairs of the business. Those customers do not have direct access to the economic statements of the business. the subsequent come below the pinnacle of external customers.

i. Banks and Financial Institutions

ii. Investors and Potential Investors

iii. Creditors

iv. Tax Authorities

v. Government

vi. Consumers

vii. Researchers

viii. Public

5. State the nature of accounting information required by long-term lenders.

Ans: Accounting information required with the aid of the long term creditors are repaying potential of the enterprise, profitability, liquidity, operational efficiency, a capacity increase of business, and so forth.

6. Who are the external users of information?

Ans: External users of statistics are the individual or the groups that have direct or indirect hobby inside the commercial enterprise firm; however, are not a part of the control. They do now not have direct access to the internal records of the firm and makes use of posted records or reports like income and loss accounts, stability sheets, annual reviews, press releases, etc. a few examples of external customers are government, tax government, exertions unions,, etc.

7. Enumerate the informational needs of management.

Ans: The informational desires of control are worried about the activities given underneath.

1. Assists in choice-making and business planning

2. Getting ready reviews associated with funds, prices and income to check the soundness of the enterprise

3. Comparing contemporary monetary statements with their very own historic monetary statements and of different similar corporations to evaluate the operational performance of the commercial enterprise.

8. Give three examples of revenues.

Ans: Three examples of revenue are given below.

1. Sales revenue

2. Interest received

3. Dividends

9. Distinguish between debtors and creditors; Profit and Gain.

Ans: The difference between Debtors and Creditors is given below.

The difference between Profit and Gain is given below.

Gain - is incidental to the business. They stand up from irregular sports or non-recurring transactions; as for instance, profit on the sale of fixed belongings, appreciation in cost of the asset, income on the sale of funding, and many others.

Profit - This refers to the excess of sales over the fee. it's far commonly classified into gross income or internet profit. net income is brought to the capital of the proprietor, which will increase the owner's capital. as an instance, items

10. ‘Accounting information should be comparable’. Do you agree with this statement? Give two reasons.

Ans: Accounting is a method of figuring out the activities of economic nature, recording them inside the journal, classifying them in their respective money owed and summarizing them in income and loss account and balance sheet and speaking outcomes to customers of such facts, viz. owner, government, creditor, traders, and so on.

According to the American Institute of Certified Accountants, 1941, "Accounting is the art of recording, classifying and summarizing in a significant manner and in terms of money, transactions and events that are, in part at least, of financial character and interpreting the results thereof."

In 1970, the American Institute of licensed Public Accountants modified the definition and stated, "The function of accounting is to offer quantitative statistics, usually economic in nature, about financial entities, this is meant to be beneficial in making monetary selections."

Targets of Accounting:

1. Recording business transactions systematically - it's miles necessary to maintain systematic records of every enterprise transaction, as it's miles beyond human capacities to bear in mind one of this large wide variety of transactions. Skipping the document of any individual of the transactions may additionally cause erroneous and defective effects.

2. Determining earnings earned or loss incurred - as a way to determine the net result on the stop of an accounting period, we need to calculate income or loss. For this reason trading and earnings and loss accounts are prepared. It offers statistics regarding how a lot of goods have been bought and offered, charges incurred and amount earned during a yr.

3. Ascertaining monetary function of the company - Ascertaining income earned or loss incurred is not sufficient; the proprietor is likewise interested by knowing the monetary role of his/her company, i.e. the fee of the assets, amount of liabilities owed, net increase or decrease in his/her capital. This reason is served by way of making ready the balance sheet that helps in ascertaining the true monetary role of the enterprise.

4. Assisting management - Systematic accounting enables the management in effective decision making, efficient control on cash management guidelines, preparing finances and forecasting, and many others.

5. Assessing the development of the enterprise - Accounting facilitates in assessing the progress of commercial enterprise from 12 months to year, as accounting allows the evaluation of each inter-company in addition to intra-company.

6. Detecting and preventing frauds and errors - it is vital to detect and prevent fraud and errors, mismanagement and wastage of the finance. Systematic recording facilitates the clean detection and rectification of frauds, errors and inefficiencies if any.

7. Communicating accounting facts to diverse users - The vital step in the accounting system is to communicate economic and accounting statistics to diverse users together with each internal and external user like proprietors, management, government, hard work, tax government, and many others. This assists the customers to understand and interpret the accounting data in a significant and suitable manner without any ambiguity.

11. If the accounting information is not clearly presented, which of the qualitative characteristics of the accounting information is violated?

Ans: If the accounting data isn't always truly offered, then the qualitative characteristics like comparison, reliability and understanding capability, are violated. that is because if the accounting information is not without a doubt provided, then the significant assessment may not be viable, as the information isn't always trustworthy, which may additionally lead to faulty conclusions.

12. The role of accounting has changed over the period of time"- Do you agree? Explain.

Ans: The role of accounting is ever converting. at the same time as in advance times, accounting became merely concerned with recording the financial events, i.e. record-maintaining activity; but, nowadays, accounting is accomplished with the rationale of no longer simplest retaining facts but additionally presenting a statistics device that provides crucial and relevant records to diverse accounting customers. The need for this alteration is delivered overdue to the ever-changing and dynamic business environment, that's more aggressive in nature now than it turned into in advance times. in addition, there are various applicable sports like decision making, forecasting, evaluation, and evaluation that make these modifications inside the function of accounting inevitable.

13. Giving examples, explain each of the following accounting terms:

- Fixed assets

- Revenue

- Expenses

- Short-term liability

- Capital

Ans:

Those are held for the long term and growth the profit incomes capability of the commercial enterprise, over numerous accounting periods. these properties are not supposed for sale; for instance, land, building, machinery, and many others.

Sales - It refers to the amount obtained from daily sports of enterprise, viz. quantity acquired from sales of products and services to customers; rent received, the commission received, dividend, royalty, interest received, and so forth. are items of sales that are delivered to the capital.

Capital - It refers to the quantity invested with the aid of the owner of a firm. it is able to be within the form of coins or belongings. it's miles a duty of the enterprise in the direction of the proprietor of the firm, in view that business is handled separate or distinct from the proprietor.

Capital = assets - Liabilities.

Costs - charges are the one’s fees that might be incurred to maintain the profitability of a commercial enterprise, like lease, wages, depreciation, interest, salaries, and so forth. those help in the manufacturing, enterprise operations and generating revenues.

Quick time period liabilities - those liabilities which are incurred with a purpose to be paid or are payable within a yr; as an instance, bank overdraft creditors, bills payable, brilliant wages, quick-time period loans, and many others.

14. Define revenues and expenses?

Ans:

Revenues - Sales discuss the amount obtained from everyday activities of the commercial enterprise, like sale proceeds of goods and rendering services to the customers. lease obtained, fee received, royalties and hobby obtained are considered as revenue, as they're regular in nature and worried with day to day activities. it is shown in the credit aspect of the income and loss account or trading account.

Expenses - Charges talk to the one’s charges which might be incurred to earn revenue for the commercial enterprise. it's miles incurred for preserving the profitability of the commercial enterprise. It shows the quantity spent to meet the quick-time period wishes of the business. it's miles shown in the debit aspect of the income and loss account or trading account. as an example, wages, lease paid, salaries paid, amazing wages, and many others.

15. What is the primary reason for business students and others to familiarize themselves with the accounting discipline?

Ans: Every economic transaction has to be recorded in such a manner that diverse accounting customers must understand and interpret these effects in an identical way with no ambiguity. The reasons why business college students and others need to familiarize themselves with the accounting field are given below.

1. It enables in studying the various aspects of accounting.

2. It enables learning how to maintain books of bills.

3. It facilitates studying how to summarize accounting data.

4. It enables in studying the way to interpret the accounting data with relative accuracy

16. What is accounting? Define its objectives.

Ans: Accounting is a process of identifying the events of financial nature, recording them in the journal, classifying them in their respective accounts and summarizing them in profit and loss account and balance sheet and communicating results to users of such information, viz. owner, government, creditor, investors, etc.

According to the American Institute of Certified Accountants, 1941, "Accounting is the art of recording, classifying and summarizing in a significant manner and in terms of money, transactions and events that are, in part at least, of financial character and interpreting the results thereof."

In 1970, the American Institute of Certified Public Accountants changed the definition and stated, "The function of accounting is to provide quantitative information, primarily financial in nature, about economic entities, that is intended to be useful in making economic decisions."

Objectives of Accounting:

1. Recording business transactions systematically - It is necessary to maintain systematic records of every business transaction, as it is beyond human capacities to remember such a large number of transactions. Skipping the record of any one of the transactions may lead to erroneous and faulty results.

2. Determining profit earned or loss incurred - In order to determine the net result at the end of an accounting period, we need to calculate profit or loss. For this purpose trading and profit and loss accounts are prepared. It gives information regarding how much goods have been purchased and sold, expenses incurred and amount earned during a year.

3. Ascertaining financial position of the firm - Ascertaining profit earned or loss incurred is not enough; the proprietor is also interested in knowing the financial position of his/her firm, i.e. the value of the assets, amount of liabilities owed, net increase or decrease in his/her capital. This purpose is served by preparing the balance sheet that facilitates ascertaining the true financial position of the business.

4. Assisting management - Systematic accounting helps the management in effective decision making, efficient control on cash management policies, preparing budget and forecasting, etc.

5. Assessing the progress of the business - Accounting helps in assessing the progress of business from year to year, as accounting facilitates the comparison both inter-firm as well as intra-firm.

17. Explain the factors, which necessitated systematic accounting.

Ans: The elements that necessitated systematic accounting are given underneath.

1. Most effective financial transactions are recorded - the one’s activities which might be monetary in nature are simplest recorded within the books of bills. as an example, the income of a worker is recorded within the books but his/her instructional qualification isn't always recorded.

2. Transactions are recorded in financial phrases - best the one’s transactions which may be expressed in financial phrases are recorded in the books. as an example, if an enterprise has two homes and 4 machines, then their economic values are recorded within the books, i.e. buildings costing Rs 2,00,000, 4 machines costing Rs 8,00,000. therefore, the whole value of belongings is Rs 10, 00,000

3. The art of recording - Transactions are recorded within the order in their prevalence.

4. Type of transaction - commercial enterprise transactions of comparable nature are categorised and published underneath their respective bills. as an instance, all the transactions relating to machinery may be published within the machinery Account.

5. Summarizing of records - All enterprise transactions are summarized within the shape of Trial stability, Trading Account, Profit and Loss Account and Balance Sheet that provides vital statistics to diverse customers.

6. Analyzing and deciphering information - Systematic accounting statistics enable customers to analyze and interpret the accounting statistics in a proper and suitable way. these accounting statistics and records are supplied within the shape of graphs, statements, charts that lead to smooth verbal exchange and understanding ability by using diverse users. moreover, these allow in decision making and destiny predictions.

18. Describe the informational needs of external users.

Ans: There are various external users of accounting who need accounting data for selection making, funding planning and assessing the economic position of the business. The diverse external users are given under.

1. Banks and other economic institutions - Banks offer finance in the shape of loans and advances to numerous businesses. thus, they want records concerning liquidity, creditworthiness, solvency and profitability to advance loans.

2. Lenders - these are the one’s individuals and companies to whom an enterprise owes money attributable to credit score purchases of products and receiving offerings; consequently, the creditors require information approximately the creditworthiness of the commercial enterprise.

3. investors and capability buyers - They invest or plan to invest in the commercial enterprise. for this reason, to be able to verify the viability and prospectus of their investment, creditors want information approximately the profitability and solvency of the enterprise.

4. Tax authorities - They need information approximately sales, sales, earnings and taxable profits if you want to decide the levy of various types of tax on the business.

5. Government - It desires records to determine national profits, GDP, industrial growth, etc. The accounting facts help the government within the formula of numerous regulations and measures and to address diverse economic problems like employment, poverty and so on.

6. Researcher - diverse research institutes like NGOs and other independent research institutions like CRISIL, inventory exchanges, etc. adopt various research tasks and the accounting records enables their studies to work.

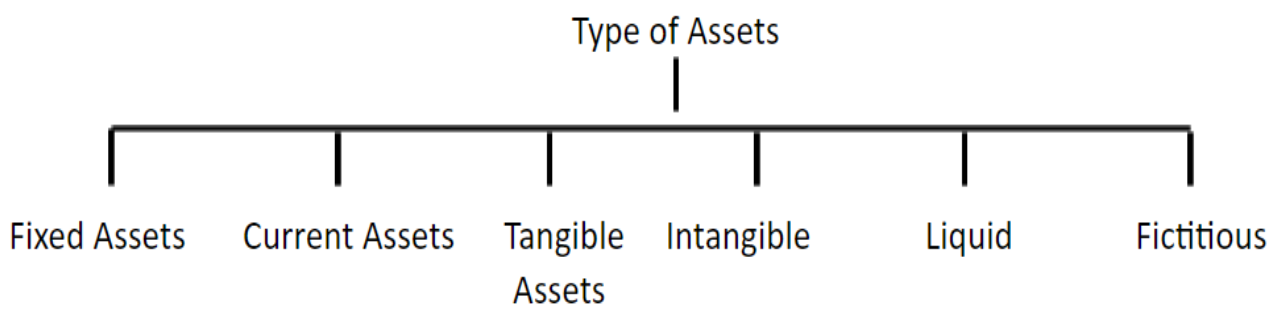

19. What do you mean by an asset and what are different types of assets?

Ans: Any valuable element that has economic value, that's owned through an enterprise, is its asset. In different phrases, the property is the financial value of the homes or the felony rights which are owned through the enterprise groups.

Fixed Assets - those are that property that is held for the long term and boom the income-earning ability and efficient capability of the business. these properties are not meant for sale, as an instance, land, constructing machinery, and so forth. current property- a property that can be without difficulty converted into coins or coins equivalents are termed as current belongings.

Those are required to run daily commercial enterprise sports; for instance, cash, debtors, stock, and many others.

Tangible belongings - a property that has physical lifestyles, i.e., which may be visible and touched, are tangible belongings; for instance, vehicles, furniture, building, and many others.

Intangible belongings - assets that can not be seen or touched, i.e. those assets that do not have bodily existence, are intangible belongings; for instance, goodwill, patents, trademark, and many others.

Liquid property - belongings that can be kept either in cash or coins equivalents are regarded as liquid belongings. these can be transformed into coins in a very brief period of time; for example, coins, financial institutions, bills receivable, etc.

Fictitious belongings - those are the heavy sales costs, the benefit of which may be derived in more than one 12 months. They constitute losses or costs which are written off over a time frame, as an example, if the commercial expenditure is Rs 1,00,000 for 5 years, then every yr Rs 2,00,000 might be written off.

20. Explain the meaning of gain and profit. Distinguish between these two terms.

Ans:

Profit - extra of revenue over rate is known as income. it is usually categorized into gross profit or internet earnings. It increases the proprietor's capital as it's far introduced to the capital at the cease of every accounting period. for example, goods costing Rs 1,00,000 are bought at Rs 1,20,000, then the sale proceeds of Rs 1,20,000 is the sales and 1,00,000 is the price to generate this sale. for this reason, an accounting profit of Rs 20,000 (i.e. Rs 1, 20,000- Rs 1, 00,000) is the distinction between the sales and price that is earned via the commercial enterprise.

Gain - It arises from irregular activities or non-habitual transactions. In other phrases, again is a result of transactions that might be incidental to the commercial enterprise, other than working transactions. for instance, antique equipment of ebook value Rs 20,000 is sold at Rs 25,000. therefore, the advantage is Rs five,000 (i.e. Rs 25,000 - Rs 20,000). here, the sale of the old equipment is an abnormal hobby; so, the distinction is termed as the benefit as a result, in different words, the best distinction between profit and benefit is that income is the excess of revenue over price and advantage arises from other than working transactions.

21. Explain the qualitative characteristics of accounting information.

Ans:

The following are the qualitative characteristics of accounting information:

1. Reliability - It method that the consumer can depend upon the accounting records. All accounting records are verifiable and can be confirmed from the supply report (voucher), viz. cash memos, bills, and so forth. subsequently, the to be had records need to be free from any mistakes and unbiased.

2. Relevance - It manner that crucial and suitable statistics have to be effortlessly and timely available and any beside the point statistics should be prevented. The customers of accounting statistics need applicable facts for selection making, planning and predicting the future conditions.

3. Understandability - Accounting records need to be supplied in this kind of manner that every person is able to interpret the facts with no difficulty in a significant and suitable manner.

4. Comparability - it's miles the most critical exceptional of accounting facts. comparability means accounting facts of a modern-day yr can be comparable with that of the previous years. comparability permits intra-company and inter-firm comparison. This assists in assessing the outcomes of numerous rules and packages followed in one-of-a-kind time horizons by means of identical or exclusive companies. similarly, it facilitates to examine the growth and development of the enterprise over time and in contrast to other companies.

22. Describe the role of accounting in the modern world.

Ans: The position of accounting has been changing over the time frame. in the cutting-edge world, the function of accounting is not most effective restricted to file monetary transactions however also offer a basic framework for various decision making, offering applicable records to numerous users and assists in each short-run and longer-term planning. the roles of accounting inside the present-day global are given underneath.

1. Supporting control - control makes use of accounting records for the brief time period and long term planning of business activities, to are expecting the future situations, prepare budgets and various manipulate measures.

2. Comparative take a look at - within the present-day world, accounting information helps us to realize the performance of the enterprise via evaluating cutting-edge 12 months earnings with that of the preceding years and also with different corporations within the equal enterprise.

3. Replacement reminiscence - within the cutting-edge international, each enterprise incurs a massive variety of transactions and it is beyond human capability to memorize each and each transaction. hence, it's miles very vital to document transactions within the books of accounts.

4. Facts to stop consumer - Accounting performs an essential role in recording, summarizing and presenting relevant and dependable statistics to its users, in the form of economic facts that enables choice making.

Topics Covered In Class 11 Accountancy Chapter 1 Introduction to Accounting

Benefits of NCERT Solutions for Class 11 Accountancy Chapter 1 Introduction To Accounting

Students develop truly from understanding how accounting is used in real-world business situations, which helps them learn the value of financial information in decision-making.

Understanding the components of equity, liabilities, and assets allows students to properly analyse financial documents and evaluate a company's financial health.

Understanding financial against management accounting prepares students for a variety of accounting careers by showing how accounting meets both external reporting and internal management needs.

Practical experience in documenting and presenting financial transactions provides students with real-life abilities that help them overcome the gap between theory and practise.

Analysing financial data helps students build critical thinking skills, allowing them to evaluate business performance and make intelligent choices.

Class 11th Accounts Chapter 1 Question Answer helps students achieve sincerity and integrity, which are required for trusted accounting practices.

Important Study Material Links for Class 11 Accountancy Chapter 1 Introduction to Accounting

Conclusion

NCERT Chapter 1 Accounts Class 11 provides a strong basis for understanding the basic principles of accounting. It introduces students to the fundamental concepts of assets, liabilities, and equity, which are necessary for understanding financial statements. Class 11th Accounts Chapter 1 Question Answer highlights the value of honesty and integrity in financial reporting. Overall, this chapter provides students with the hands-on expertise and moral values required for overcoming the difficulties of accounting in the business sector.

NCERT Solutions for Class 11 Accountancy (Part - I) - Other Chapter-wise Links - FREE PDF

Download our FREE PDF links offering chapter-wise NCERT solutions prepared by Vedantu Master teachers, to help you understand and master the social concepts.

Related Important Links for Class 11 Accountancy

FAQs on NCERT Solutions For Class 11 Accountancy Chapter 1 Introduction To Accounting - 2026-27 Free PDF Download (Login Required)

1. How can one download the introduction to accounting NCERT PDF solutions for Class 11?

Visit the Vedantu NCERT Solutions page for Class 11 Accountancy Chapter 1. Locate the "Download PDF" button and click it to save the file. Use this for offline access to all questions and answers, ensuring you can study anywhere, anytime without an internet connection.

2. How do you identify a business transaction in accounting?

Identify any economic event that changes the financial position of a business, involving assets, liabilities, or equity. Ensure it is measurable in monetary terms. For example, purchasing goods for cash is a transaction, but a manager's skill is not, as it cannot be monetarily valued.

3. What is a simple way to distinguish an asset from a liability?

Define an asset as a resource the business owns that provides future economic benefit (e.g., cash, machinery). Define a liability as an obligation the business owes to others (e.g., loans, creditors). An asset adds value; a liability is a claim on assets.

4. How can one use NCERT solutions for a quick revision of Chapter 1?

Scan the solutions for key definitions and solved problems. Focus on the final answers of numerical questions to quickly check your own work. This helps reinforce concepts from the class 11 accountancy chapter 1 question answer section without re-reading the entire chapter.

5. What is the primary objective of accounting?

The main objective is to systematically record financial transactions and events to ascertain the profit or loss for a period and the financial position of the business on a specific date. This information is then communicated to interested users like investors and management.

6. How should one use the NCERT Solutions for Class 11 Accountancy Chapter 1 to practice different types of questions?

Use the NCERT Solutions for Class 11 Accountancy Chapter 1 by first attempting all the exercise questions from the textbook on your own. This helps you identify areas where you need more clarity.

7. How can one explain the four qualitative characteristics of accounting information?

Explain the qualitative characteristics by defining each one and providing a simple business context. These characteristics—Reliability, Relevance, Understandability, and Comparability—are the attributes that make accounting information useful to its users.

Reliability: Describe it as information that is free from error and bias, meaning it is verifiable and factual. For instance, a sales invoice backs up a revenue entry.

Relevance: Explain that information is relevant if it influences the decisions of users, helping them predict outcomes or confirm past evaluations.

Understandability: Define this as information presented in a clear and concise manner so that users with reasonable business knowledge can comprehend it.

Comparability: Explain that information must be comparable over time and with other businesses to identify trends and performance benchmarks.

8. What is an effective way to use the Free PDF of NCERT Solutions for offline study?

Download the Free PDF to create a dedicated study resource that you can access on any device without needing an internet connection. This is perfect for focused, distraction-free learning sessions.

Once downloaded, integrate the PDF into your study routine. Use it alongside your NCERT textbook to cross-reference questions and answers instantly. This makes it easier to tackle the introduction to accounting questions and answers class 11.

9. What are the steps to define the role of accounting in a modern business?

Define the role of accounting by breaking it down into its core functions, which extend beyond simple bookkeeping. Accounting acts as the language of business, providing critical information for decision-making, control, and legal compliance.

Understanding its role helps appreciate why introduction to accounting class 11 NCERT solutions focus on systematic recording and reporting. It shows how accounting supports business strategy.

10. How does one determine if an event is a financial transaction that should be recorded in accounts?

Determine if an event is a recordable financial transaction by applying the "money measurement concept." An event must meet two key criteria to be recorded in the books of account.

First, check if the event affects the financial position of the business (i.e., changes the value of assets, liabilities, or capital). Second, ensure this change can be measured and expressed in monetary terms.