How to Find Rate of Interest in Simple Interest with Formula and Solved Examples

The rate of interest is the percentage of principal that a lender charges to a borrower. Different banks provide different rates of interest. Simple interest is very commonly used in our daily lives. The rate of interest is always taken as a fraction in the formula for simple interest. In this article, we will discuss about what is simple interest and the formula for calculating simple interest.

What is Simple Interest?

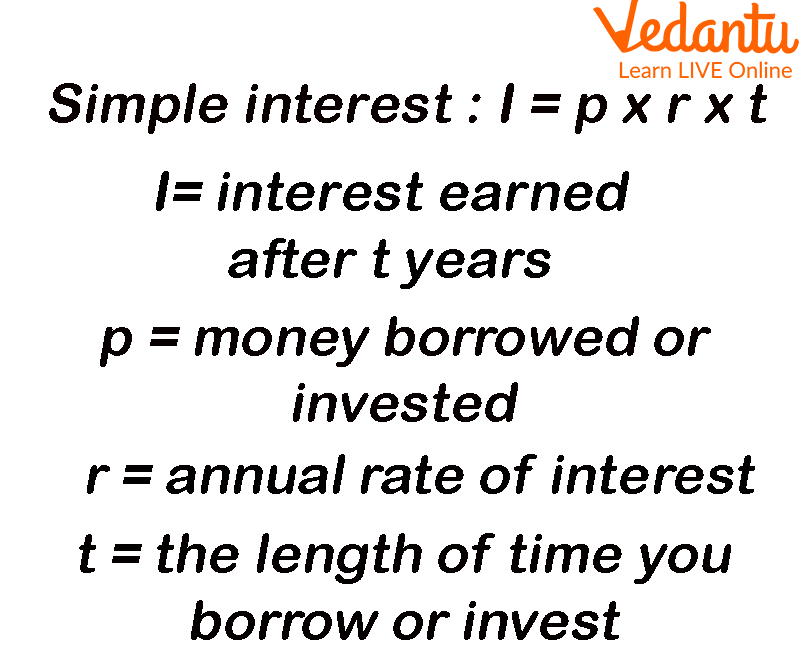

Before we learn the formula for rate in simple interest, we will first learn what simple interest is. Simple interest is a method to calculate the interest gained over a particular sum, at a specific rate in a given period of time. The interest is applied on the amount (principal) you invest in the bank at a fixed interest rate. The formula for calculating simple interest is \[\]\[\left[ {{\text{simple interest}}} \right] = \left[ {{\text{Principal}}} \right] \times \left[ {{\text{percent rate of interest per annum}}} \right] \times \left[ {{\text{time}}} \right]\].

Simple Interest

The Formula for Simple Interest

Simple interest is simply calculated using the following formula.

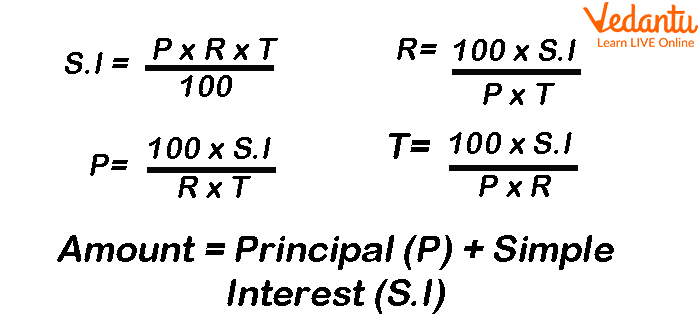

\[{\rm{S}}{\rm{.I = P}} \times {\rm{R}} \times \dfrac{T}{{100}}\] (As R is in percent)

Here, S.I. = Simple interest

\[{\text{p = principal amount }}\]

R = rate of interest in % per annum

T = The duration for which the money is invested.

Amount = It is the total money gained after the investment duration is over. It is calculated as \[{\text{Amount = Principal + Simple Interest }}\]

Formula for Simple Interest and Its Components

Rate of Interest in Simple Interest

The rate of interest is the percentage of principal that a lender charges to a borrower. A 5% rate of interest means you will be charged 5% of the amount you have invested/ loaned from the lender, each year for the given time period. For example, a 2% rate of interest on Rs. 100,000 for 4 years means you will be charged 2% of 100,000 which is 2,000 per year for 4 years. The simple interest here will be \[{\rm{S}}{\rm{.I = 100000}} \times {\rm{[2\% ]}} \times {\rm{4 = 8000}}\]. Thus, the total payable amount will be \[{\text{Principal + }}\] \[{\rm{S}}{\rm{.I = 100000 + 8000}}\] = Rs. 108,000.

The Formula for Rate of Interest in Simple Interest

These are the steps to find the rate of interest.

We first start with a formula for simple interest.

Then we make the rate of interest the subject of the equation and isolate it.

This will give us the formula for the rate of interest. Remember that the rate of interest is always kept a fraction in formulas.

Rate of interest %= \[\dfrac{\text{Simple interest}}{\text{principal} \times \text{time}}\]

Simple Interest and Its Components

We have learned about simple interests and their components. We have successfully understood the formula of simple interest and how its components work. We learned how the rate of interest practically works and how to calculate the rate of interest from the formula for simple interest.

Solved Examples

1. Find the rate of interest if the simple interest is given to be Rs. 4,000 on a principal of Rs. 50,000 for 2 years.

Solution: We are given simple interest, principal amount, and the time period. We are required to find the rate of interest. Using the formula for rate of interest in the simple interest, we get

\[\dfrac{R}{{100}} = \dfrac{{[{\rm{S}}{\rm{.I]}}}}{P \times T}\]

\[\dfrac{R}{{100}} = \dfrac{{\left[ {4000} \right]}}{{\left[ {50000 \times 2} \right]}}\]

The above equation gives

\[\dfrac{R}{{100}} = 0.04\]

Hence, \[R = 4\% \]

2. Find the rate of interest if the total amount at the end of the interest period is given to be Rs. 640,000 on the principal amount of Rs. 500,000 for 7 years.

Solution: We start with writing down the formula for the amount.

\[{\text{Amount = principal + simple interest}}\]

\[{\text{Amount = principal + principal}} \times {\rm{rate}} \times {\rm{time}}\]

Now we put down the values we already have been given,

\[640000 = 500000 + 500000 \times \dfrac{R}{{100}} \times 7\]

or,

\[\dfrac{R}{{100}} \times 7 = \dfrac{{140000}}{{500000}} = \dfrac{{14}}{{50}}\]

\[\dfrac{R}{{100}}= \dfrac{2}{{50}} = 0.04\]

This gives,

\[R =4\% \]

Conclusion

Simple interest is very commonly used in our daily lives. Banks use this method daily to provide loans to customers. We have learned how important simple interests are and how we can calculate them. We also learned how to calculate different components (Principal, Rate of interest, and time period) if any three of the quantities are given.

FAQs on Rate of Interest in Simple Interest Explained with Formula

1. What is the rate of interest in simple interest?

The rate of interest in simple interest is the percentage charged or earned on the principal amount per year. It shows how much interest is paid for every ₹100 (or $100) in one year. In simple interest, the rate remains constant throughout the time period and is usually expressed as a percentage per annum (p.a.).

2. What is the formula for rate of interest in simple interest?

The formula for the rate of interest (R) in simple interest is R = (SI × 100) / (P × T).

- SI = Simple Interest

- P = Principal amount

- T = Time (in years)

3. How do you calculate the rate of interest when simple interest is given?

You calculate the rate of interest by using the formula R = (SI × 100) / (P × T).

- Step 1: Write the given values of SI, P, and T.

- Step 2: Substitute them into the formula.

- Step 3: Simplify to get R.

R = (500 × 100) / (2000 × 2) = 50000 / 4000 = 12.5%.

4. What is the simple interest formula?

The simple interest formula is SI = (P × R × T) / 100.

- P = Principal

- R = Rate of interest (per annum)

- T = Time in years

5. How do you find the rate of interest if the amount is given?

To find the rate when the amount is given, first calculate simple interest using SI = A − P, then apply R = (SI × 100) / (P × T).

- Step 1: Find SI by subtracting principal from amount.

- Step 2: Substitute SI, P, and T into the rate formula.

R = (200 × 100) / (2000 × 2) = 5%.

6. What is the difference between rate of interest and simple interest?

The rate of interest is the percentage charged per year, while simple interest is the actual money earned or paid.

- Rate (R) is expressed in percentage (%).

- Simple Interest (SI) is expressed in currency.

- Rate helps calculate SI using the formula SI = (P × R × T) / 100.

7. Can the rate of interest be calculated if time is in months?

Yes, convert time in months into years before using the formula for rate of interest.

- Time in years = Months / 12

- Then apply R = (SI × 100) / (P × T)

8. What happens to simple interest if the rate of interest increases?

If the rate of interest increases, the simple interest increases proportionally. Since SI = (P × R × T) / 100, SI is directly proportional to R.

- If R doubles, SI also doubles.

- If R decreases, SI decreases in the same ratio.

9. How do you find the rate of interest per annum?

The rate of interest per annum is found using R = (SI × 100) / (P × T in years). Ensure time is expressed in years before calculation. The result gives the annual rate as a percentage (% p.a.).

10. What are common mistakes when calculating rate of interest in simple interest?

Common mistakes when calculating the rate of interest in simple interest include incorrect substitution and wrong time conversion.

- Not converting months into years.

- Forgetting to subtract principal from amount to find SI.

- Using the wrong formula.

- Missing the multiplication by 100 in R = (SI × 100) / (P × T).