How to Use the Formula to Calculate Simple Interest with Examples

When one deposits money in a bank, the bank applies to interest on the money deposited. Banks use various types of interest, and one of them is simple interest. Simple Interest is a quick and easy way to calculate the interest on your money, where interest is always applied to the principal at the same rate for each time period. Simple interest is determined by multiplying the principal by the daily interest rate by the number of days elapsed between payments.

What is Simple Interest?(Simple Interest Definition)

Interest is the income you receive from deposits or fees you pay on loans.

Simple Interest is a measure of interest that does not account for interest or accruals over multiple periods. The interest rate applies only to the principal of the loan or investment and is not affected by interest accrued.

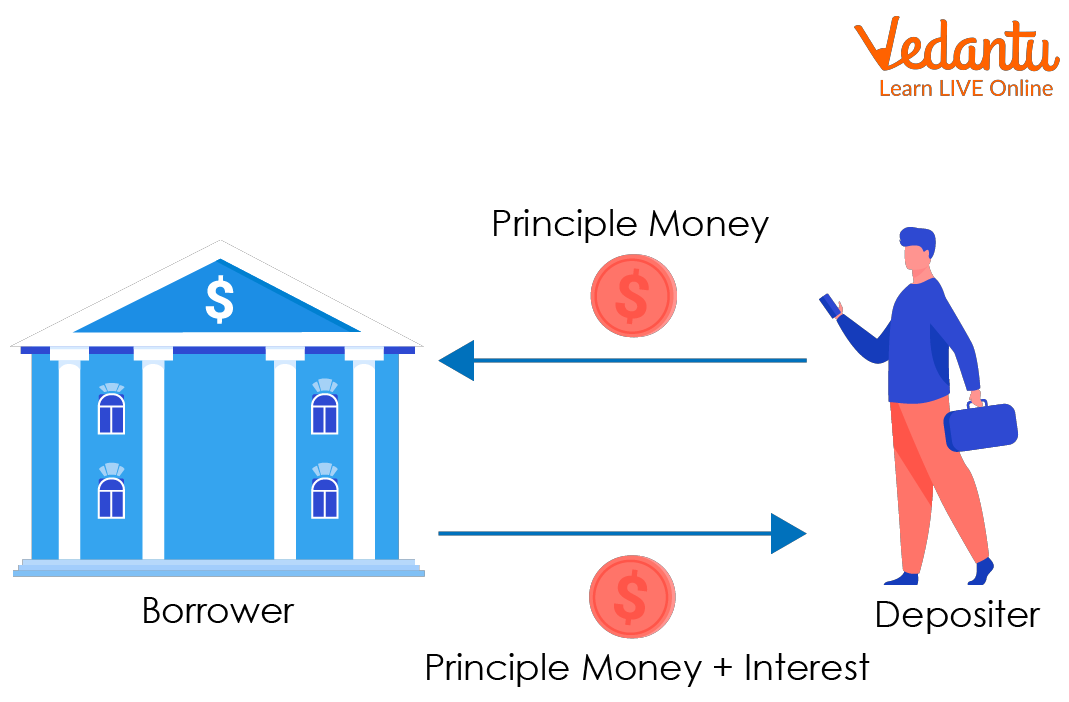

Simple Interest

How to Find Simple Interest?

Simple Interest is calculated by using the formula:

\[{\rm{SI}} = {\rm{P}} \times {\rm{R}} \times {\rm{T}}\]

Where,

P = Principal

R=Percentage rate of Interest per annum [year]

T=time taken in the year

Simple Interest Formula Example

Terms Related to Simple Interest

Some terms like Principal, rate and time used to find Simple Interest. Let’s discuss each:

Principal: The amount borrowed from the bank by a person is called the Principal. The head is designated by the letter P.

Rate: The interest rate is the interest rate at which the principal is paid to someone over a period of time, which could be 5% or 15% etc. The interest rate is denoted by R.

Time: Time is a period given to someone on the principal amount. Time is indicated by the letter T.

Amount: When you get a loan from a bank, you must repay the principal plus interest, and this repayment is called the amount. So, a sum of money at simple interest amounts to the money you have to pay back. The amount is denoted by A.

Thus \[{\rm{A = P + I}}\]

Conclusion

On a specific principal, simple interest remains constant year after year. Consider the day you must return the money, not the day you borrowed it, to determine the amount of time. The interest rate is always given as a fraction in the formula.

Solved Examples

1. If the principal is Rs. 2500 for 1 year at the rate of 15%.Calculate simple interest.

Solution: Using the simple interest formula

\[{\rm{SI}} = {\rm{P}} \times {\rm{R}} \times {\rm{T}}\]

Here P \[ = \]2500, T \[ = \]1year and \[{\rm{R}} = 15\% \left[ {\frac{{15}}{{100}}} \right]\]

So in the above value

\[{\rm{SI}} = 2500 \times \frac{{15}}{{100}} \times 1\]

\[{\rm{SI}} = 375\]

So, simple interest is 375.

2.Mohan pays back 7,000 rupees equal to 5,000 rupees borrowed over two years. Find the interest rate.

Solution: A \[ = \]7000rupees

P \[ = \]5000rupees

We know \[{\rm{A}} = {\rm{SI}} + {\rm{P}}\]

\[{\rm{SI}} = {\rm{A}} - {\rm{P}}\]

\[{\rm{SI}} = {\rm{A}} - {\rm{P}} = 7000 - 5000 = 2000\] rupees

T \[ = \] 2years

Also

\[{\rm{SI}} = \frac{{[{\rm{P}} \times {\rm{R}} \times {\rm{T}}]}}{{100}}\]

\[{\rm{R}} = \frac{{100{\rm{SI}}}}{{{\rm{P}} \times {\rm{T}}}}\]

\[{\rm{R}} = \frac{{[100 \times 2000]}}{{[5000 \times 2]}}\]

\[{\rm{R}} = 20\% \]

So ,\[{\rm{R}} = 20\% \]

3. Naman borrowed Rs 20,000 for 3 years at an interest rate of 3% per annum. Find of the accumulated interest at the end of 3 years.

Solution: P \[ = \]20,000rupees

\[{\rm{R}} = 3\% \]

T \[ = \]3years

\[{\rm{SI}} = \frac{{[{\rm{P}} \times {\rm{R}} \times {\rm{T}}]}}{{100}}\]

\[{\rm{SI}} = \frac{{[20000 \times 3 \times 3]}}{{100}}\]

\[{\rm{SI}} = 1800\]

Therefore accumulated interest at the end of 3 years is 1800

FAQs on Simple Interest Formula and Calculation Method

1. What is the formula to calculate simple interest?

The formula to calculate simple interest is SI = (P × R × T) / 100.

- P = Principal amount

- R = Rate of interest (per annum)

- T = Time (in years)

2. What is simple interest in Maths?

Simple interest is the interest calculated only on the original principal amount for the entire time period. It does not include interest on previously earned interest. In basic mathematics and finance, simple interest is commonly used for short-term loans and banking calculations.

3. How do you calculate simple interest step by step?

To calculate simple interest, use the formula SI = (P × R × T) / 100 and follow these steps:

- Step 1: Write down the principal (P), rate (R), and time (T).

- Step 2: Multiply P × R × T.

- Step 3: Divide the result by 100.

SI = (5000 × 6 × 2)/100 = 600.

4. What is the amount formula in simple interest?

The amount formula in simple interest is A = P + SI. Since SI = (P × R × T)/100, the amount can also be written as:

A = P(1 + RT/100).

- A = Final amount

- P = Principal

5. Can you give an example of a simple interest calculation?

Yes, a simple interest example is: If 8000 is invested at 5% per annum for 3 years, the interest is calculated using SI = (P × R × T)/100.

- SI = (8000 × 5 × 3)/100

- SI = 1200

6. What is the difference between simple interest and compound interest?

The main difference is that simple interest is calculated only on the principal, while compound interest is calculated on principal plus accumulated interest.

- Simple Interest Formula: SI = (P × R × T)/100

- Compound Interest Formula: A = P(1 + R/100)T

7. How do you find the rate of interest in simple interest?

The rate of interest in simple interest is found using R = (SI × 100) / (P × T).

- SI = Simple Interest

- P = Principal

- T = Time in years

8. How do you calculate time in simple interest?

The time period in simple interest is calculated using T = (SI × 100) / (P × R).

- SI = Simple Interest

- P = Principal

- R = Rate of interest

9. What are the units used in the simple interest formula?

In the simple interest formula, the principal is in currency, the rate is in percent per annum, and time is in years.

- P = Rupees/Dollars/etc.

- R = % per year

- T = Years

10. What are common mistakes when calculating simple interest?

Common mistakes in simple interest calculations include using incorrect units and forgetting to divide by 100.

- Not converting months into years.

- Using rate as a decimal instead of percentage without adjusting the formula.

- Forgetting the formula SI = (P × R × T)/100.